In today’s competitive rental market, being a landlord requires diligence, attentiveness, and savviness, especially when selecting who’ll be living on your property.

After all, the last thing you want to experience is endless quarrels with your tenants about unpaid rent and having to serve and enforce a slew of eviction notices!

In your quest to separate the risky tenants from the safe ones, it’s always wise to perform a credit check on each applicant. It’s a foundational component of the tenant screening process. It’ll pay for itself over time by helping you identify quality candidates – one that’ll make rent payments like clockwork.

While these checks provide valuable insight into prospective tenants, even seasoned landlords can overlook crucial details. Thus, it’s always worth reminding yourself of the items to look for when evaluating credit reports. That way, you can quickly pinpoint the red flags, as well as easily identify a solid tenant.

SingleKey offers an excellent way for landlords to screen tenants via our Tenant Credit & Background Check. We’ve helped landlords across Canada screen and verify thousands of prospective tenants, providing valuable details that make renting a far less risky and hassle-free experience. To help you learn how to read the SingleKey tenant screening report, we’ll review the top 5 tenant credit check metrics.

Don’t forget to check out our sample tenant credit check report. We’ll be using it as a reference throughout this article.

How to Read a Credit Report for Landlords: 6 Key Tips

1. Know the Difference Between Poor, Good, and Great Credit Score

The first indicator you should review is the applicant’s credit score. This financial metric measures their creditworthiness or the riskiness of lending money to them. In Canada, credit scores range from 300 to 900, with the average hovering around 630. Though primarily used by lenders, a credit score is also valuable data for landlords. It paints an accurate picture of a tenant’s history with credit and how responsible they are when it comes to payments. In Canada, two private firms assign credit scores to individuals: Equifax and TransUnion. Both organizations collect and store borrowers’ credit data and incorporate it into complex scoring models to calculate their scores. Here’s a breakdown of what components go into a credit score and the relative importance of each. If an applicant possesses a high credit score, they handle debt responsibly and make timely payments. Naturally, this is a favourable attribute, as they’ll have little or no trouble paying their rent on time. On the other hand, a low credit score indicates the applicant has a history of poor debt management and is more likely to default on the payment obligations. As a result, you should think twice about offering them tenancy, as they may fall behind on their rent easily. Since the average Canadian has a credit score of 630, you should review rental applicants with scores below this number with greater scrutiny. A credit score below 500 likely stems from an excessive debt load, numerous missed payments, or a recent bankruptcy, suggesting a high-risk applicant. SingleKey uses an Equifax ER 2.0 score to create an accurate profile of a tenant’s financial health. Here’s a snapshot that shows what you can expect from each report: While a low credit score doesn’t mean that a tenant will be delinquent on rent, we can safely assume that a tenant who fails to pay their bills on time is more likely not to pay their rent on time.2. Assess the Tenant’s Payment Habits

As a landlord, you want tenants who’ll diligently keep up with their rent payments, so you want to take a peek into their payment history. Lenders report consumer debt payments to Equifax and TransUnion whether they’re late, on time, or missed entirely. Thus, all will have an impact on an applicant’s credit report. Specific sections of our report that relate to an applicant’s payment history include:- Past due amount – the amount they owe on a particular credit account(s).

- Payments 30/60/90 – the number of times they made a payment late by 30 days, 60 days, and 90 days.

- Payment status – shows whether they’re current or behind with their payments.

- Last payment – shows the date of the last payment made.

3. Identify The Type of Debt Of Debt The Tenant Owes

Another critical detail on our credit report is the type of debt an applicant is responsible for servicing. While an immense debt load of any type can be troubling, it’s essential to understand that not all debt is equal. Some debt products are inherently riskier than others. High-Interest Debt High-interest debt comes with greater risk because the tenant can quickly become overwhelmed with interest charges and struggle to make timely payments. Lenders typically charge high interest rates on loans where the borrower has not pledged an asset as collateral. Examples include credit cards, payday loans, and unsecured lines of credit. Low-Interest Debt Low-interest debt poses much less risk for the tenant. Since they accrue few interest charges, making debt payments is more manageable. In addition, an asset typically secures these loans, which provides an extra layer of security should the tenant default. Examples of low-interest debt include mortgages, home equity lines of credit, and auto loans.4. Tally Up the Tenant’s Monthly Debt Payments

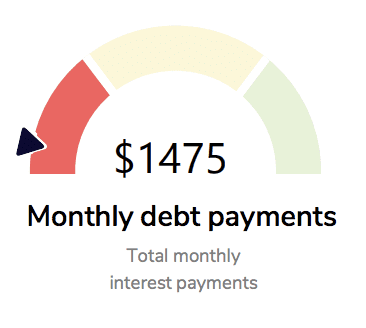

Credit reports outline the number of regular payments a person has to pay towards an auto loan, credit card, cell phone, etc. It’s important to review these monthly payments because you can determine what percentage of the applicant’s income goes toward covering recurring expenses and bills. For example, in SingleKey’s sample credit report, the “Payment Term Amount” shows how much the applicant must pay, and the “Narrative” explains the frequency of payments Naturally, the higher their debt burden, the greater the chance they’ll encounter issues making prompt payments, which increases your risk as a landlord. For example, suppose an applicant earns a pre-tax income of $3,000 per month but pays $1,000 in credit card and car loan payments every month. In that case, they’ll have little funds left over to cover rent and living expenses.5. Calculate The Rent To Income Ratio

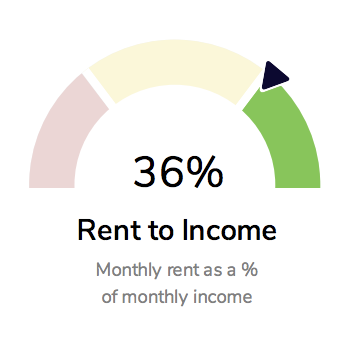

It’s important to know if an applicant can afford to rent your unit. Thus, you should examine their monthly income and determine what percentage would cover rent. Luckily, SingleKey’s tenant credit report calculates the rent-to-income ratio for each applicant, so you won’t have to worry about crunching the numbers yourself. Evaluating tenants’ rent-to-income ratio allows you to gauge affordability. If an applicant earns $3,000 per month but is applying to rent a unit that costs $2,000 per month, that’s a red flag. Many landlords prefer to rent to tenants with a rent-to-income ratio no higher than 30%. This figure is a good rule of thumb to keep in mind when deciding whether or not to consider a particular applicant. However, studies show that the 30% threshold is not attainable for many individuals. As a result, it’s not uncommon for landlords to accept 50% or higher rent-to-income ratios. Still, our data shows affordability is one of the top predictors of tenant rent default. If tenants spend more than 50% of their income on rent, they risk having insufficient funds to dedicate to rent payments. In this scenario, unexpected expenses or job loss would cause the tenant to stop paying rent. Thus, it’s wise to be patient and seek out tenants with ratios closer to 30%. We also suggest going one step further and using the (rent + debt payments) to income ratio. With this formula, you combine the tenant’s monthly debt obligations and rent to better grasp how much they can afford.

6. Focus on Derogatory Marks

A derogatory mark is a negative item on a credit report that has significant long-lasting financial repercussions for an individual’s credit standing. Here are some scenarios that can cause one to appear on an applicant’s credit report- Their credit card provider issued a charge-off on a past due balance

- They filed for bankruptcy

- A creditor has sent their account to a collection agency

- A creditor has repossessed their home or car due to a default