- Tenant Report, International Tenants

- 20 Minute Read

Equifax vs TransUnion: What landlords should know for tenant screening

Updated on Jul 20, 2026

Written By:

Verified By:

Equifax and TransUnion are separate credit bureaus. Each uses distinct credit-scoring algorithms and has its own policy for collecting and managing credit information. As a result, two credit reports for the same applicant can look surprisingly different. For example, SingleKey found that credit scores differed by more than 40 points in 42% of cases.

Neither credit bureau is inherently better or more accurate than the other. But understanding how and why their credit reporting differs can help you make smarter decisions about tenant selection. In this article, we’ll break down the key differences between Equifax and TransUnion and why it’s wise to use both when screening tenants.

Equifax vs TransUnion at a glance

Equifax and TransUnion operate in the same industry and share the same goal of collecting, processing, and reporting credit information. Below is a comparison of the two from a landlord’s perspective, highlighting the similarities and differences.

Swipe horizontally to view the complete comparison.

| Area | Equifax | TransUnion | Landlord takeaway |

|---|---|---|---|

| Credit-scoring model | Equifax Risk Score 3.0 and customized FICO models | CreditVision and VantageScore models | Scores can differ even when based on similar information. SingleKey found differences over 40 points in 42% of cases. |

| Credit history considered | 81 months | 84 months | Different scoring windows can produce different scores. |

| Data sources | Information reported to Equifax | Information reported to TransUnion | Reviewing only one bureau may leave out an account. SingleKey found a 55% chance of this happening. |

| Hard inquiries retained | 3 years | 6 years | Hard inquiries remain visible longer on TransUnion reports. |

| Positive information retained | Indefinitely, or 10 years for closed accounts | 20 years | A longer positive history may contribute to a stronger score. |

| Negative information retained | Up to 6 years | Up to 6 years; some bankruptcies remain longer | What appears may vary by bureau and province. |

Equifax vs TransUnion for tenants vs landlords

Credit reports are vital to both landlords and tenants during the screening process. Both parties care about what information the report communicates. However, they have different priorities, which can lead them to prefer one credit bureau over the other.

What tenants look for

Tenants primarily care about the accuracy of their credit reports, especially if they manage their money responsibly. The reason is that an up-to-date, accurate credit report increases the chance of securing a tenancy.

For example, let’s say a tenant owes on a car loan and routinely pays on time. In that case, they would expect to see all of their on-time payments on their report with no errors or omissions.

In addition, tenants are concerned about which credit bureau a landlord checks. The reason is that one may paint them in a more favourable light, giving them an edge over other applicants.

In Canada, rent-payment information may be reported to Equifax, TransUnion, or both, depending on the rent-reporting provider. A tenant who has worked to build their credit history through rent reporting may prefer that a landlord review the bureau file where those payments appear.

What landlords look for

Landlords are primarily concerned with an applicant’s payment history and the amount of debt they owe relative to their income. These metrics allow them to assess the risk that an applicant will fail to pay rent on time. However, landlords also examine other factors during the screening process, such as employment stability, background checks, and references from past landlords.

Which credit bureau do landlords use?

In Canada, landlords may use Equifax, TransUnion, or both. When running a credit check on tenants , practices vary: some landlords prefer one credit bureau, while others review reports from both agencies to get a more complete picture of each applicant.

What we found comparing hundreds of Equifax and TransUnion reports

At SingleKey, we analyzed hundreds of Equifax and TransUnion credit reports to see how the two compare in the information they provide. Below is a summary of our key findings to help you decide whether to use one or the other, or both, for screening tenants.

Credit scores

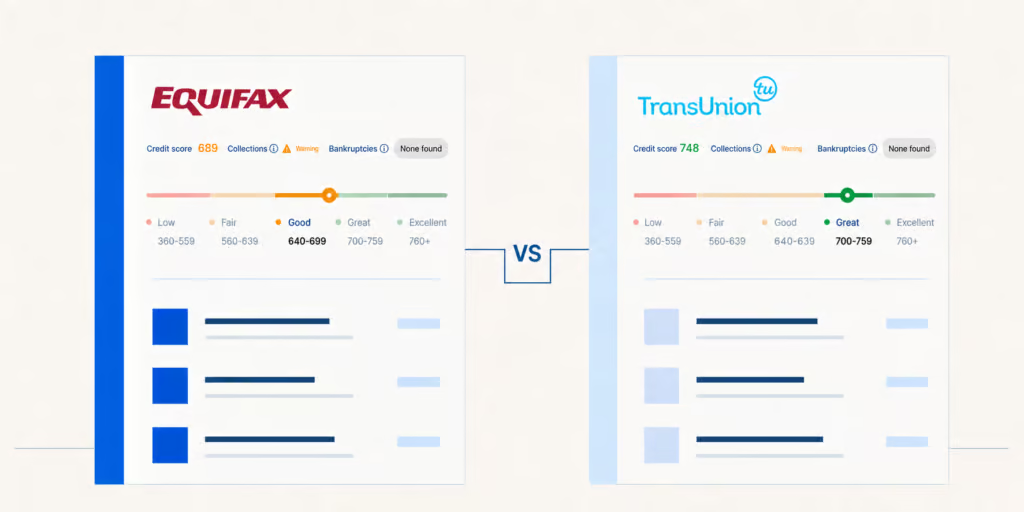

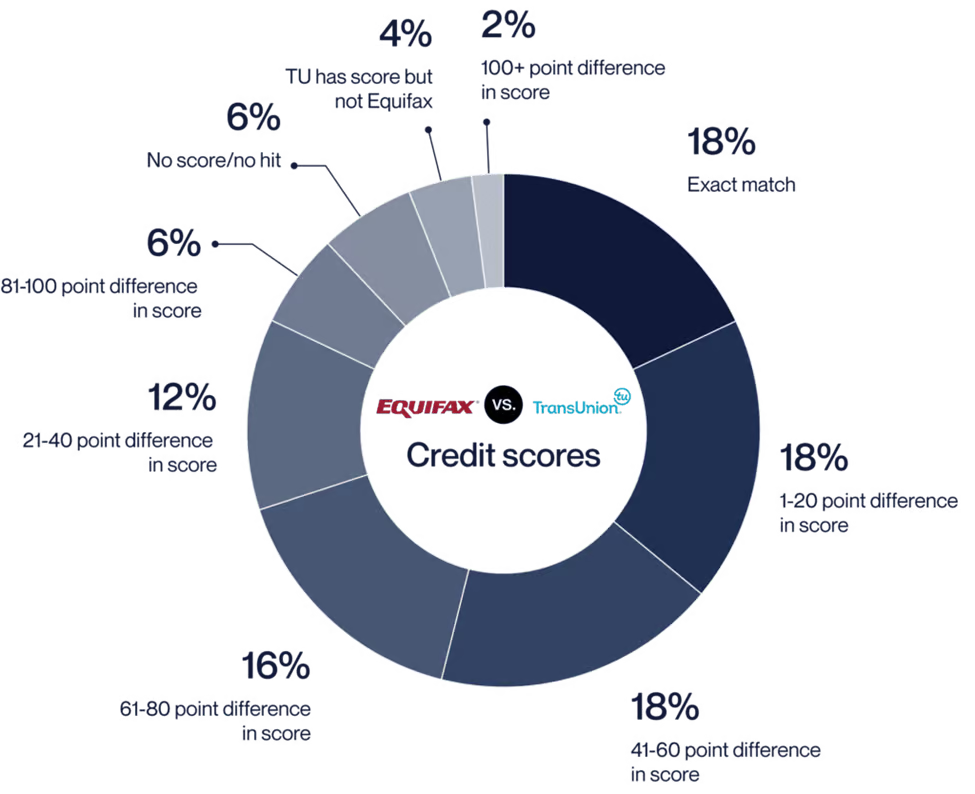

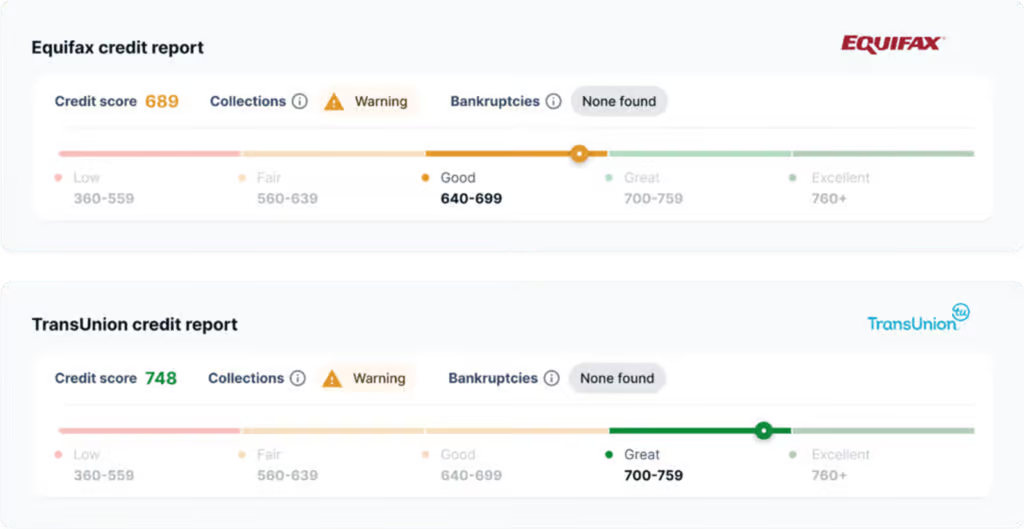

Our analysis found that Equifax and TransUnion reported different credit scores for applicants. An exact match occurred only 18% of the time, and TransUnion scores were generally higher than Equifax scores.

The size of these differences was particularly notable. In 34% of paired reports, scores differed by 41–80 points. Overall, 42% differed by more than 40 points, and one pair was 142 points apart.

Depending on where the scores fall, a gap like this could affect whether an applicant is selected, as the example below illustrates.

Total debt

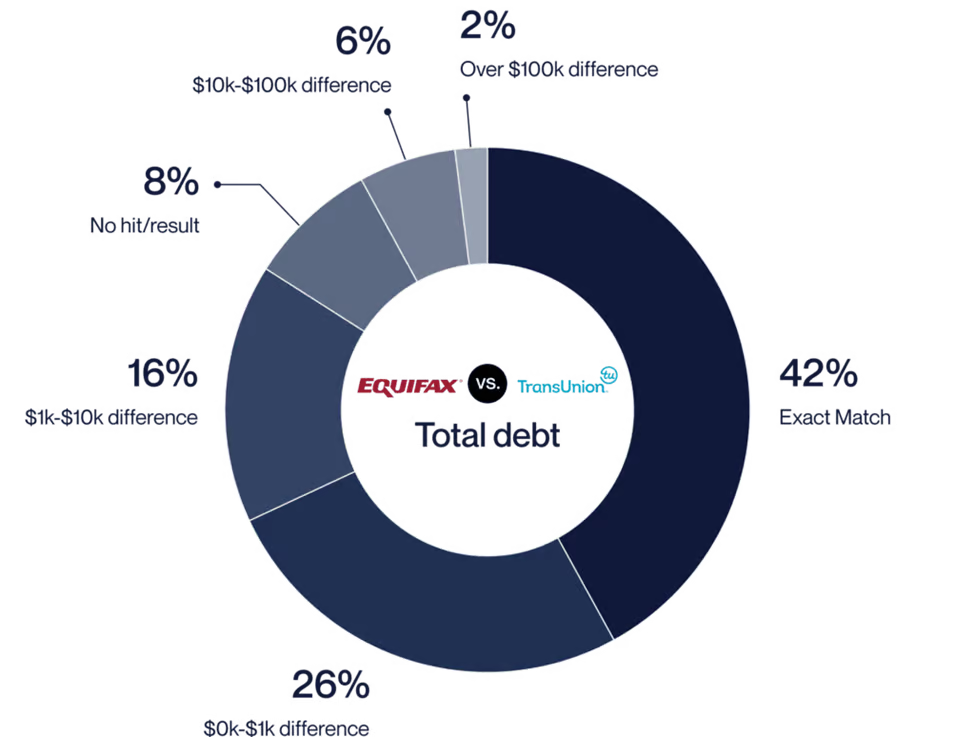

For total debt owed, we found an exact match only 42% of the time. In 26% of cases, the disparity between Equifax and TransUnion was negligible, anywhere from $1 to $1,000. However, in some cases, it was substantial: 6% of paired reports showed a difference of up to $10,000. On average, the difference in debt between the two reports was $16,171.

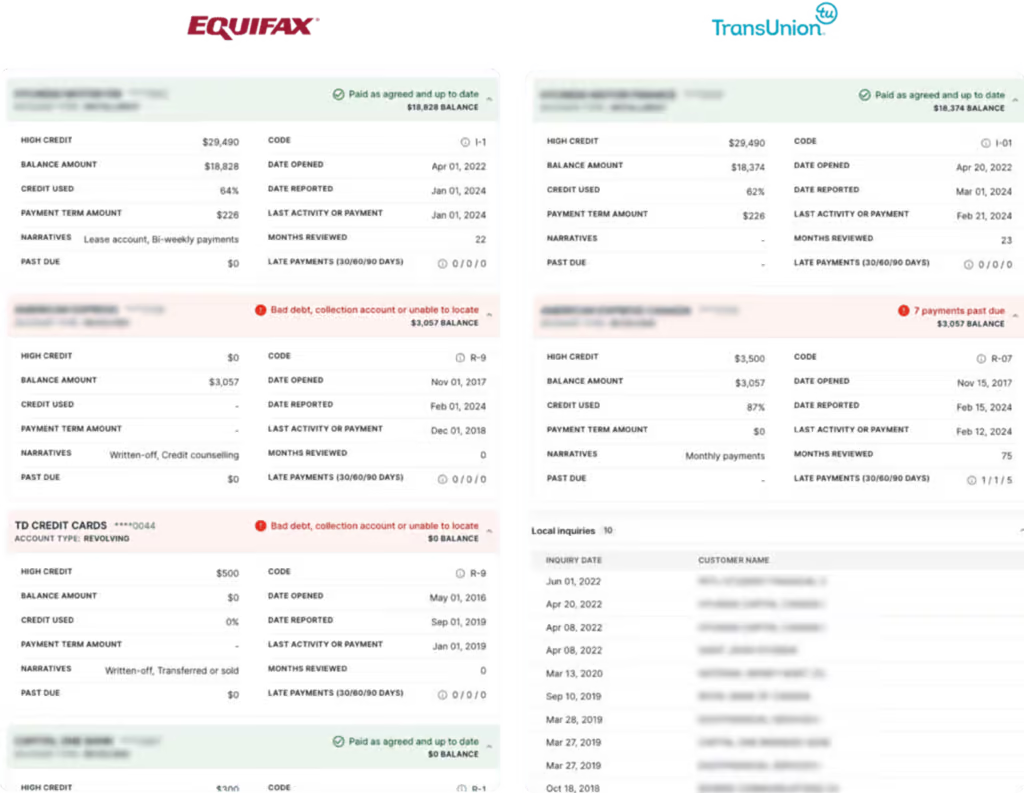

Tradelines

Tradelines are credit accounts listed on a credit report, such as personal loans, credit cards, and lines of credit. In theory, an applicant’s tradeline history across Equifax and TransUnion reports should be identical. But that’s not the case.

On average, we found a difference of 3.7 tradelines reported between the two bureaus. Overall, TransUnion credit reports displayed more tradelines and more historical data than their Equifax counterparts. Here’s an example in which Equifax showed an overdue tradeline, while TransUnion did not report the same tradeline.

Collections

When looking at accounts in collections, our analysis found that both Equifax and TransUnion reported these unpaid debts 59% of the time. That means there’s a 41% chance that an account sent to a collection agency won’t appear on a credit report from one bureau.

We also found an average of 1.3 differences in non-matching collections. TransUnion had a small advantage because it returned slightly more collections.

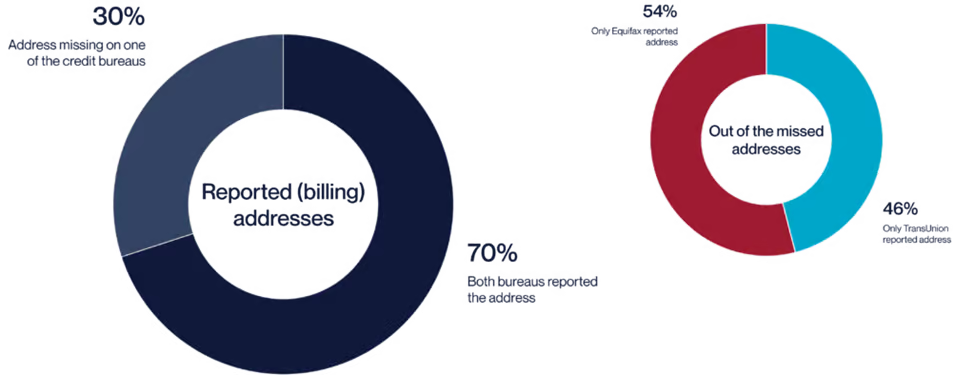

Address history

Reported addresses are those used for billing when an individual opens a product or service, such as a cell phone or a streaming service. Based on our data, we found that 70% of legitimate addresses appeared on the reports of both credit bureaus. Of the 30% of addresses missing, 54% were reported only to Equifax and 46% to TransUnion, giving Equifax a slight advantage.

Employment history and inquiries

While Equifax and TransUnion report on a person’s employment history and any related inquiries, we found that this data rarely matched between the two credit bureaus.

Why Equifax and TransUnion scores and reports don’t always match

Here are some of the main reasons credit histories and scores on an Equifax report may not align with those on a TransUnion report.

-

Not all lenders report to both bureaus. A lender, credit card issuer, or collection agency may choose to report to only one credit bureau. They are not obligated to report to both, which means certain details found on one credit file may be absent from the other.

-

Creditors may report to each bureau at different times. A recent payment or balance change may appear on one report before it appears on the other, depending on when the lender or creditor sends the update.

-

Credit-scoring models differ. Equifax and TransUnion each have distinctive formulas for calculating credit scores. As a result, discrepancies between reports can occur even if both bureaus collect and process the same credit information.

-

Some accounts may appear in only one report. Even when a type of information can be reported to both bureaus, a specific account may appear in only one file depending on the reporting provider, participation, and timing.

-

Credit bureaus update their records at different times. Equifax and TransUnion follow different schedules for updating credit data they receive, which can result in temporary differences between reports.

-

Reports may contain errors. Occasionally, a credit report from one bureau may contain duplicate accounts, incorrect balances, or outdated information. These errors and updates can remain on file for a long time before they are discovered.

-

Personal information may be recorded differently. Variations in a person’s name, address, and other identifying information can affect whether a credit account is matched to a tradeline in the credit file.

As our study shows, there’s a high probability that financial data from one credit bureau will not match the other. That’s why it’s good to pull reports from Equifax and TransUnion to ensure you don’t miss any critical details. One report can miss something that the other captures.

SingleKey’s Tenant Report combines Equifax and TransUnion data in one easy-to-read dual-bureau credit report, providing a more complete view of a potential tenant’s credit history.

Can landlords get a credit report directly from Equifax or TransUnion?

Landlords can obtain a credit report directly from Equifax and TransUnion. To do this, you must set up a commercial account with one or both bureaus. This option is a safe and reliable way to access credit reports for tenant screening. But it can be cumbersome, time-consuming, and costly, especially for large rental portfolios.

Opening a commercial account often requires an extensive vetting process, business verification, site inspections, and training on the credit bureau’s online portal. You may also incur high fees for each report ordered on an ad hoc basis.

Another option is to order SingleKey’s Tenant Report . The Tenant Report combines Equifax and TransUnion data into a single, easy-to-read document. There’s no hard pull on the applicant’s credit score, and applicant consent is built directly into the workflow.

This can be a faster and more affordable solution because SingleKey already has established commercial relationships with Equifax and TransUnion. You can skip the paperwork and verification the credit bureaus typically require.

You can also ask applicants to provide their own credit reports, which can save you time and money. But there are significant risks with accepting credit reports directly from tenants .

What landlords should look for in a tenant credit report

Landlords should review a credit report as a whole to understand how well the applicant can handle their financial obligations, not just the credit score or other metrics in isolation. Here are some key items to review in a credit report to learn if an applicant is capable of paying rent on time.

| Credit report item | Why it matters to landlords |

|---|---|

| Payment history | A consistent track record of on-time payments is a strong indicator that the tenant is likely to pay on time. |

| Credit score | A high credit score suggests the tenant repays debts they owe, so they have a lower risk of default. Always consider the credit score alongside the rest of the credit report. |

| Outstanding debt | High levels of debt decrease financial flexibility, making it harder to cover rent payments. |

| Credit utilization | A high credit utilization suggests the tenant relies heavily on credit, which can make it harder to keep up with rent. |

| Collection accounts | Accounts in a collection agency may hint at financial issues that merit further investigation to learn how the tenant is currently managing their money. |

| Public records, if reported | Certain records, such as court judgements and liens, may provide helpful information about a tenant’s financial standing. |

| Length of credit history | A long and positive track record of using credit products demonstrates financial responsibility. |

| Types of credit accounts | A mix of credit accounts indicates the tenant has experience handling various financial obligations. |

| Recent credit inquiries | Multiple hard inquiries over a short period may be a sign that the tenant is desperately seeking new credit or is in financial trouble. |

| Bankruptcies or consumer proposals, if reported | Bankruptcies and consumer proposals point to severe financial distress, increasing the risk of unpaid rent, though it’s important to consider when they took place. |

Learn more about what landlords should look for in a credit report during the tenant screening process.

Ready to do a credit check on a promising applicant? Order SingleKey’s Tenant Report today to access valuable credit information pulled directly from Equifax and TransUnion. Applicant consent is built into the flow and there’s no hard pull on the applicant’s credit score.

Learn more about Tenant Report

Learn more about Tenant Screening

- Greatest Fears in Property Management

- How to Screen Tenants Like A Pro (Checklist Included)

- SingleKey Survey: Challenges with Screening Tenants

- How Do Landlords Screen Tenants?

- What is Rental Arbitrage and What Are the Risks for Landlords?

- 9 Questions Landlords Need to Ask Potential Tenants

- Everything You Need to Know About Tenant Screening Laws in Canada

- 5 Tips to Streamline the Rental Application Process

- What Should Landlords Look for in A Tenant Credit Report?

- Decoding the SingleKey Tenant Screening Report

- Good Tenant Bad Credit: What You Need to Know

- 3 Reasons Landlords Shouldn’t Accept Credit Reports Directly from Tenants

- What is an R Code? Credit Report Codes Explained

- Equifax vs TransUnion: What landlords should know for tenant screening

- Rent-to-Income Ratio Calculator: A Handy Tool for Landlords

- How to Verify Employment History for Potential Tenants

- Questions You Need to Ask in a Landlord Reference Check

- A Landlord’s Guide to Rental Verification

- A Landlord’s Guide to Spotting Fake Rental Applications

- How Landlords Decide on Approving Tenants

- What is a Good Credit Score?