- Tenant Screening

- 4 Minute Read

What is an R Code? Credit Report Codes Explained

Updated on Sep 1, 2025

Written By:

Verified By:

As a landlord, it’s crucial to analyze a rental applicant’s credit report before considering them as your tenant. You may have seen codes like “R2” and “I5” and wondered what they mean.

In this guide, we’ll explain the most common credit report codes, what they represent, and why they matter to you as a housing provider.

What are credit report codes?

Credit report codes, or credit ratings, are unique combinations of a letter and a number that credit bureaus use to describe how and when individuals make debt payments. Some lenders and creditors also use these ratings when providing financial information to credit bureaus.

In other words, credit report codes grade an individual’s payment history, which has a major impact on their credit score. As such, lenders heavily rely on these codes to help them decide whether to loan money to a borrower. Landlords also use them to understand a potential tenant’s ability to handle rent payments.

Credit report codes defined

The letter in a credit report code describes the type of credit product the individual uses, and the number represents the account’s payment status. Below are the most common codes and what they mean:

Letter

Type of Account

Example

O

Open status credit. The individual can access credit at their discretion up to a predetermined credit limit. Payments will vary based on the amount borrowed and the lender’s terms.

Line of credit

R

Revolving credit. The individual can borrow money up to a predetermined credit limit. Payments will vary based on the amount borrowed and the lender’s terms.

Credit card

I

Installment loan. The individual borrows money for a specific period and repays the balance through fixed payments.

Car or student loan

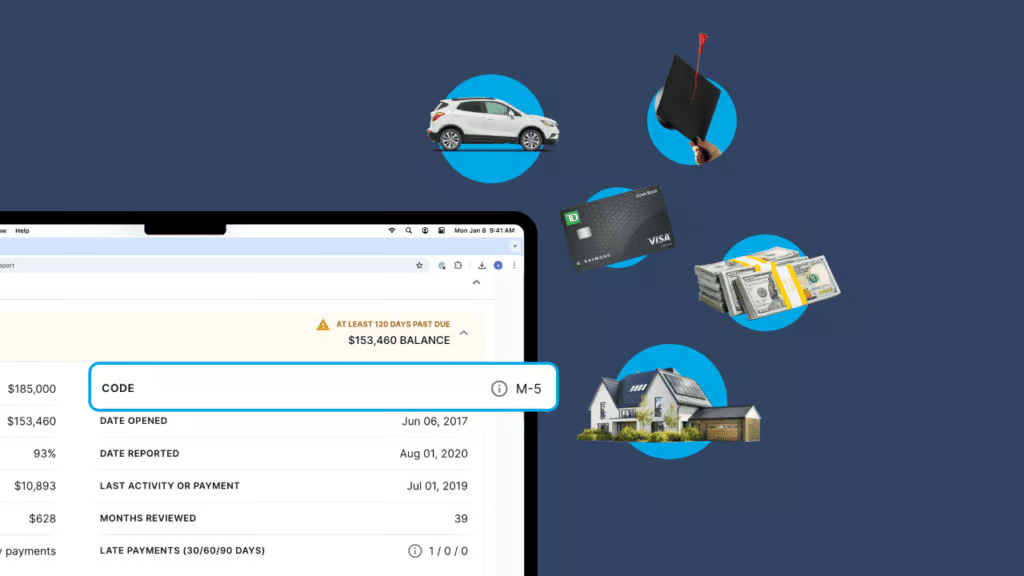

M

Mortgage loan. A mortgage may not always appear on a credit report. Mortgages are repaid through regular fixed payments based on an amortization schedule.

Residential mortgage

Number

Definition

Interpretation

0

Approved and opened recently so there’s no payment history to report

New account

1

Paid off within the agreed-upon time period (usually within 30 days of the billing date)

Very good

2

Payment made between 31 and 59 days late

Note and assess with other tenant screening criteria

3

Payment made between 60 and 89 days late

Potential red flag

4

Payment made between 90 and 119 days late

Potential red flag

5

Payment made more than 120 days late

Potential red flag

6

This code isn’t used by credit bureaus

N/A

7

Regular payments made under a consolidation order, consumer proposal, or debt management program (DMP)

Red flag

8

Lender is attempting to repossess the borrower’s assets to cover the amount owed

Red flag

9

The debt has been written off, sent to a collection agency, or the borrower has filed for bankruptcy

Major red flag

Let’s say you’re evaluating a rental applicant’s credit report and see the code R1. That means the individual has a credit card and is making on-time payments. What if you discover an I4 code? In that case, they’re responsible for some installment loan, perhaps a car loan, and they made at least one payment between 90 and 119 days late.

As you can see, the lower the number associated with an account, the better the individual is at meeting payment deadlines.

Why is understanding credit report codes important?

Understanding credit report codes can help you assess a tenant’s financial stability. Do they pay their bills on time? If not, how often do they fall behind on payments? Is it one specific account that’s giving them trouble, or all of them?

Credit report codes can provide you with answers to these questions during the tenant screening process. As a result, you may have a better shot at finding a renter who can meet their financial responsibilities.

Our final thoughts

Credit report codes are a handy shortcut for learning about an individual’s payment history. They’re part of the many factors that help determine if your prospective tenant will be able to make timely rent payments. Learn more about how to read a credit report to help you find a great tenant for your rental.

Learn more about Tenant Screening

Learn more about Tenant Screening

- Greatest Fears in Property Management

- How to Screen Tenants Like A Pro (Checklist Included)

- SingleKey Survey: Challenges with Screening Tenants

- How Do Landlords Screen Tenants?

- What is Rental Arbitrage and What Are the Risks for Landlords?

- 9 Questions Landlords Need to Ask Potential Tenants

- Everything You Need to Know About Tenant Screening Laws in Canada

- 5 Tips to Streamline the Rental Application Process

- What Should Landlords Look for in A Tenant Credit Report?

- Decoding the SingleKey Tenant Screening Report

- Good Tenant Bad Credit: What You Need to Know

- 3 Reasons Landlords Shouldn’t Accept Credit Reports Directly from Tenants

- What is an R Code? Credit Report Codes Explained

- Equifax vs. TransUnion: What a Landlord Needs to Know

- Rent-to-Income Ratio Calculator: A Handy Tool for Landlords

- How to Verify Employment History for Potential Tenants

- Questions You Need to Ask in a Landlord Reference Check

- A Landlord’s Guide to Rental Verification

- A Landlord’s Guide to Spotting Fake Rental Applications

- How Landlords Decide on Approving Tenants

- What is a Good Credit Score?