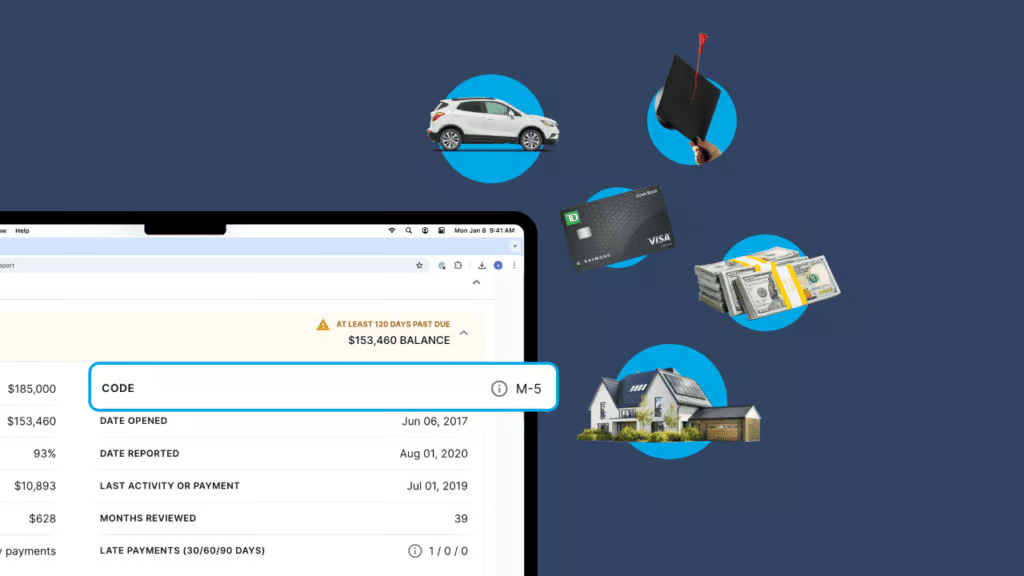

Let’s say you’re evaluating a rental applicant’s credit report and see the code R1. That means the individual has a credit card and is making on-time payments. What if you discover an I4 code? In that case, they’re responsible for some installment loan, perhaps a car loan, and they made at least one payment between 90 and 119 days late.

As you can see, the lower the number associated with an account, the better the individual is at meeting payment deadlines.

Why is understanding credit report codes important?

Understanding credit report codes can help you assess a tenant’s financial stability. Do they pay their bills on time? If not, how often do they fall behind on payments? Is it one specific account that’s giving them trouble, or all of them?

Credit report codes can provide you with answers to these questions during the tenant screening process. As a result, you may have a better shot at finding a renter who can meet their financial responsibilities.

Our final thoughts

Credit report codes are a handy shortcut for learning about an individual’s payment history. They’re part of the many factors that help determine if your prospective tenant will be able to make timely rent payments. Learn more about how to read a credit report to help you find a great tenant for your rental.