- Finance Management

- 11 Minute Read

How to Fill Out a T776 Form (Tax on Rental Income)

Updated on Feb 27, 2025

Written By:

Verified By:

Managing a rental property can be a great way to generate a stable income and grow your wealth. Remember though that rental income is taxable. You must declare and pay tax on your rental earnings to the Canada Revenue Agency (CRA) by completing a T776 form, also known as the Statement of Real Estate Rentals.

Learn how to fill out a T776 form to manage your rental expenses, minimize your tax bill, and avoid penalties from the CRA.

What is a T776 Form, Statement of Real Estate Rentals?

Any revenue generated from renting a property is subject to income tax in Canada. You must report your total net profit (income minus expenses) or loss to the CRA each calendar year.

Form T776 is used to report income and expenses related to renting out real estate and providing basic amenities like heat, parking, and appliances.

Submitting this form isn’t mandatory: you’re free to disclose your income and expenses using your own financial statements. However, the CRA encourages property owners to use the T776 form. We recommend doing the same, especially if you’re starting out as a landlord.

Mac's Pro Tip

Step by step: How to complete the T776 form

Access the T776 form here, then use our breakdown below to complete the form. You can also use the following links to go to each section:

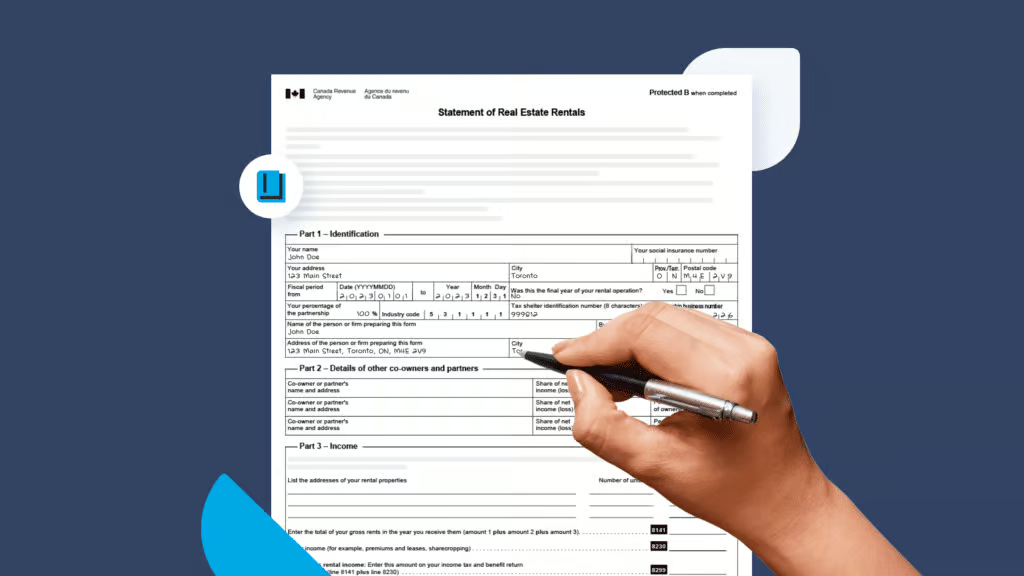

Part 1 – Identification

In Part 1, you provide general details about yourself and your rental operation.

Start by entering your name, address, city, province, postal code, and social insurance number (SIN). Next, complete the following:

Fiscal period

For tax reporting purposes, the fiscal year for rental properties always starts on January 1 and ends on December 31. The only exception would be during your first year of operations. If your property was available for rent on May 15, you would enter this date in the “from” field. All subsequent years would use the period from January 1 to December 31.

Was this the final year of your rental operation?

Will you be shutting down your rental business in the current tax year? If so, choose “Yes.” If not, select “No.”

Tax shelter identification number

A tax shelter is an investment arranged in a way that reduces the amount of tax you owe to the CRA. If you have a tax shelter identification number, enter it in the field provided. You can find this eight-digit number on your T5013 slip.

Partnership business number

Fill out this field only if you operate your rental with one or more individuals. Enter your partnership business number here, which consists of nine digits. Then, provide your percentage share of the business in the field directly to the left of the tax shelter identification number.

Name and address of person of firm preparing this form

Will someone else be preparing form T776 on your behalf? If so, enter their name and address in this area.

Business number or account number

In this section, provide your 15-character RZ account number if you have one. It has three parts:

This is a unique number that identifies your business. It’s also the same one you enter in the “partnership business number” field if you earn rental income through a partnership.

This code specifies the type of business activity reported to the CRA. In this case, your program account code is “RZ,” which applies to information-based returns like the T776 form.

This number references the individual program account (businesses can have multiple program accounts that are the same).

Part 2 – Details of other co-owners and partners

Complete this section only if you co-own the rental property with another person or operate it as a partnership with them. Fill out your co-owner’s or partner’s name, address, share of the income or loss for the year, and their percentage of ownership in the property.

A co-owner is someone with whom you share ownership of the rental property, typically your spouse or common-law partner.

In some cases, the co-owner qualifies as a partner. The CRA defines a partner as two or more people engaged in a business activity to generate a profit, either with or without a formal agreement.

As such, co-owning a rental unit with someone doesn’t automatically mean they’re your partner. To learn more about whether a relationship constitutes a partnership, check out Income Tax Folio S4-F16-C1, What is Partnership?

Part 3 – Income

The first thing you’ll notice in Part 3 are instructions to use the accrual method when calculating your total rental income and expenses.

Under the accrual method, you record income when it’s due (in this case, the first day of each month) instead of when the money arrives in your bank account.

Conversely, under the cash method, you record income only when you receive the funds. While the CRA prefers that you use the accrual method, it’s okay to use the cash method to keep things simple.

Enter the address of your rental property, the number of units it contains, and the gross income earned (income before deducting expenses).

Next, fill out the following areas as needed:

Enter the total amount you received from tenants by cash or cheque.

If your tenant pays for their rent through means other than cash, enter the fair market value of the good or service provided on this line.

In this area, you also enter the total income earned from any other sources related to your rental property, such as subleasing or sharecropping.

Determine your total gross rental income by adding the figures from lines 8141 and 8299. You enter this amount on line 12599 of your tax return.

Mac's Pro Tip

You can deduct unpaid rent from your gross rental income. Doing so will lower your tax liability.

Part 4 – Expenses

In Part 4, you deduct eligible expenses you incurred from running your property:

At the top of Part 4, there’s a list of expenses you can claim, such as insurance, management fees, and property taxes. Enter the total for each under the appropriate line, then add the lines to determine your total expenses for the year. Enter this figure on line A.

If you live in the property you rent out, only the portion of expenses related to the rented area are tax-deductible. Figure out how much applies to your personal use and how much to your tenant. Examples of expenses you must distribute are electricity bills and property taxes.

Assess your expenses and record the personal portion under the appropriate line. Add the lines and enter the total on line 9949. Subtract the figure from line 9949 to arrive at your allowable expense deduction, and enter the amount on line 4.

Enter the difference between your gross income and allowable expenses (line 8299 minus line 4). This amount is your net rental income. If you’re a co-owner or partner, ensure you input only your share.

In this line, you can enter eligible expenses you didn’t claim elsewhere on Form T776 due to being a co-owner or partner. Otherwise, you can skip it.

You may only need to fill out this part if you sell your rental property or other assets it contains.

According to the CRA, recaptured capital cost allowance occurs when the amount of money you get from the sale of depreciable property is more than the total of both of the following:

- The undepreciated capital cost (UCC) of the class at the beginning of the year

- The capital cost of any additions made during the year.

In simple terms, if the proceeds from the sale are more than the initial cost of the property and the additions you made to the property, the difference is considered taxable income.

A terminal loss is the exact opposite of recaptured capital cost allowance. In this scenario, you sold an entire class of assets for less than you initially paid to acquire them (plus the cost of any additions and improvements). You can claim the loss as an expense on line 9948.

Like recaptured capital cost allowance, the only time you may encounter a terminal loss is by selling your rental property or various assets it contains, such as appliances and furniture.

Capital cost allowance (CCA) is a tax deduction that accounts for depreciation. Depreciation is the loss in value of an asset due to wear and tear. It’s a distinct expense you can claim after deducting all other expenses like utilities, property taxes, and office costs.

You must complete Area A of the T776 form to determine your CCA deduction.

You can report any GST/HST rebate you received that relates to a partnership here. This rebate allows you to recover a portion of the GST/HST paid for qualifying expenses.

In this area, you can report any other eligible expenses you have as a partner that you didn’t deduct elsewhere.

This is the final step for calculating your taxable rental income. Enter the amount from line 9, which you get after deducting all expenses from your total rental earnings. The resulting figure represents your net income or loss of the year. You must report this figure on line 12600 of your tax return.

If you’re a partner, add line 9974 and subtract line 9943 from line 9 to determine your net income or loss.

Area A – Calculation of capital cost (CCA) claim

Area A is where you calculate capital cost allowance (CCA), otherwise known as depreciation. Each year, you can claim a maximum amount of CCA as an expense to account for the gradual loss of value of your rental assets, including the building itself.

Here’s how to calculate CCA in a nutshell:

- Step 1: Determine what CCA classes your assets belong to.

- Step 2: Sort each asset according to its class and then add the total you paid to purchase them.

- Step 3: Multiply the total cost of each class by its CCA rate and then add the results together.

- Step 4: The result is the allowable CCA you can deduct as an expense for the year.

Once you figure out your allowable CCA, enter the number on line 9936 of form T776.

The rules and mechanics behind CCA can be tricky to navigate, even for seasoned landlords. For more details about its calculation, visit the CRA’s in-depth guide on how to complete the capital cost allowance (CCA) charts. If you need more help, consider hiring a tax expert.

Areas B, C, D, E, and F

If you’ve purchased or sold rental property assets during the year, fill out the applicable sections from B to F before completing Area A.

List furniture, appliances, fixtures, yard equipment, and other property purchased for your rental. Don’t forget to include improvements. Substantial repairs that extend an item’s useful life are also eligible for CCA.

List any new rental units you acquired during the current year, plus any improvements or additions, such as a kitchen renovation or roof replacement.

The same types of items that belong in Area B can be listed here. The only difference is that these are the ones you’ve sold. Include in this area the total proceeds you received from the sale.

In this area, record any rental properties you sold during the year and the total proceeds received.

Enter the amount you paid to acquire land or received after selling it. Land doesn’t qualify for CCA, so always exclude it when determining your deduction.

Our final thoughts

At first glance, a T776 form looks intimidating: it’s five pages long with multiple sections of jargon. To simplify the task of completing it, assemble all the details you need, such as your business account number, list of expenses, and assets eligible for CCA.

If you need assistance or have questions about specific sections, consult an accountant or other tax expert. While the CRA provides the T776 form online, you can also create it automatically through your tax software. To learn more about managing your taxes as a landlord, visit our financial management resources.

Learn more about Finance Management

Learn more about Finance Management

- Tax on Rental Income: A Guide for Canadian Landlords

- The Essential Rental Property Expense Sheet

- How to Calculate Depreciation on Rental Property in Canada (And How to Claim It)

- How to Calculate Rental Property Depreciation in the U.S.

- What Rental Income Expenses Can You Claim on Your Tax Return as a Landlord?

- Capital Improvements vs. Repairs: What to Know for Your Rental Property Taxes

- How to Fill Out a T776 Form (Tax on Rental Income)

- A Guide to Reporting Rental Income: How to File a Schedule E

- Can A Landlord Claim a Rental Loss from Unpaid Rent?

- How Tenants Can Claim Rent on Their Tax Return

- Part 1: Accounting for Rental Properties: Common mistakes and how to avoid them

- Part 2: Accounting for Rental Properties: When to hire a bookkeeper or accountant

- Mastering a Mortgage Renewal: A Guide to Financial Confidence (Calculators Included)

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in Canada?

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in the United States?

- How to Calculate Rent and Get the Best Rent Estimate