- Finance Management

- 9 Minute Read

A Guide to Reporting Rental Income: How to File a Schedule E

Updated on Sep 24, 2025

Written By:

Verified By:

Whether you manage a dozen condo units or rent out the basement of your home, it’s your responsibility as a landlord to declare your rental earnings to the IRS by using the tax form Schedule E (Supplemental Income and Loss).

In this guide, we’ll explain how Schedule E works, who has to file it, and what information you need to fill it out correctly.

What is Schedule E?

Schedule E is a tax form where you report income and expenses related to real estate property, royalties, partnerships, S corporations, trusts, estates, and real estate mortgage investment conduits (REMICs).

If you earned income from renting out real estate, you must complete Schedule E and attach it to Form 1040 when filing your taxes. Form 1040 is the standard document most taxpayers use to report their personal income to the federal government.

The IRS regularly updates any changes to Schedule E in their instructions for completing it.

Who should complete a Schedule E?

You’re legally obligated to fill out and submit Schedule E if you earned an income from renting out real estate. However, the reporting requirements vary depending on whether you’re an individual investor, partner, or shareholder in an S corporation.

The IRS considers you an individual investor if you rent out your primary residence or one or more properties you own. This designation applies whether you rent out a spare bedroom in your family home or collect rent from multiple tenants in an apartment complex.

If this definition describes you, report the total rental income earned during the tax year on Schedule E in Part I. Of course, you can also deduct all eligible expenses.

Partnerships and S corporations are distinct legal entities for tax purposes. As such, they must report their rental income and expenses using Form 8825.

If you hold an ownership interest in a partnership or S corporation, any income or loss is passed on to you. Disclose this by filling out Part II of Schedule E.

Before filling out Schedule E, your company must issue a Schedule K-1. This document summarizes the year’s income or loss to shareholders or partners.

You don’t need to file Schedule K-1 with your personal tax return: the partnership or S corporation will file a copy with the IRS instead. The only exception is if box 13, code B, shows backup withholding. If so, submit Schedule K-1 when filing your taxes. Either way, keep a copy of this form for your records.

There are two other documents you may need as references when completing Part I:

- Form 8582: This form lets you calculate your allowable loss from a rental property.

- Form 4562: You can use this form to determine your Section 179 expense, a special deduction available for purchases of specific depreciable property.

When should I file a Schedule E?

Schedule E accompanies your primary tax return, so you should submit it by mid-April, which is the tax filing deadline for most taxpayers. If you file an extension, you’ll have until mid-October to send it.

Filing Schedule E can be more complicated if your rental income stems from a partnership or S corporation. Companies usually wait until mid-March to issue Schedule K-1s. Further delays mean the document could arrive quite late, which is entirely possible as Schedule K-1 forms are notorious for arriving late. If you need more time, file Form 4868 to extend your deadline.

How do I fill out each section of Schedule E?

Below is an overview of the four sections of Schedule E and how to complete them. Remember that you only need to fill out the part that applies to your tax scenario.

Use the links below to go to the section that relates to you:

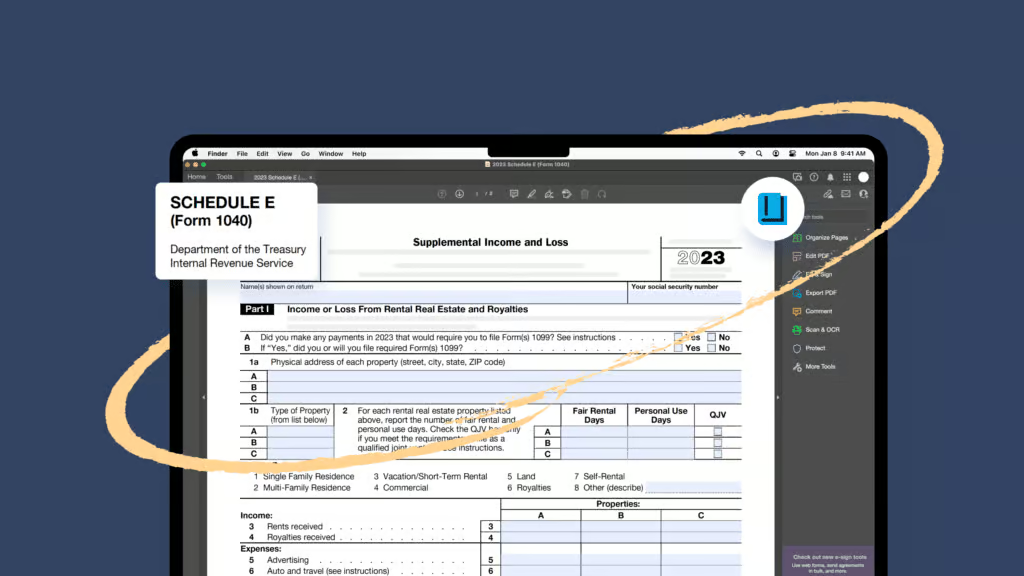

Part I: Income or Loss from Rental Real Estate and Royalties

In Part I, you declare rental income and expenses from rental real estate (and royalties, if you have any). It’s likely the only section you’ll have to complete if you own and rent out properties as a sole proprietor.

Provide your rental address, property type, and the number of days it was rented out (fair rental days) during the year. The last point is crucial, as it determines what amount, if any, of your expenses you can claim as a deduction.

Only costs related to the rented-out portion are tax-deductible. The IRS generally deems a property a home rather than a rental if personal usage exceeds 14 days or 10% of the total days rented at the market price. If these conditions apply to you, you cannot deduct any expenses.

Enter your total rental income in the “Rents received” field. Remember to include application fees, security deposits withheld from tenants, and any other income earned related to your property.

Eligible expenses

Part I provides a list of eligible expenses you can deduct. Be sure to claim every cost you can to minimize your tax liability, including depreciation on your building. You can find a comprehensive breakdown of allowable rental property expenses and how to calculate them in IRS Publication 527.

Before recording your expenses, gather all your receipts to ensure you capture all your deductions. Include your mortgage interest if you’re financing your property (your bank will send you form 1098, which summarizes your total interest paid).

You may need to file form 1099-MISC if you’ve made payments to independent contractors over $600. If that’s the case, check “Yes” on Line A.

Part II: Income or Loss From Partnerships and S Corporations

If your rental business is structured as a partnership or S corporation, complete Part II instead of Part I.

Report only your share of the income or loss. To complete Part II accurately, you’ll need to review your Schedule K-1. It should contain instructions for transferring the necessary information to Schedule E on your tax return.

Some details you’ll need to provide in Part II are your company’s name, whether it’s a foreign partnership, and an employment insurance number (EIN).

Sometimes, the IRS may reduce or disallow a rental loss if it’s excessive. There are rules you must apply to a loss before claiming it, some of which apply strictly to partners and others to S corporations. Be sure to read the instructions for Schedule E for further details or speak with your accountant.

Part III: Income or Loss From Estates and Trusts

Part III of Schedule E deals with beneficiaries of an estate or trust. Much like a partnership or S corporation, you’ll receive a Schedule K-1, showing your income or losses, which may relate to rental properties. Follow the instructions outlined in this form to report the items correctly in Part III.

Passive activity loss rules may apply if your estate or trust incurred a loss. These rules prevent taxpayers and legal entities from deducting substantial losses, particularly those from rental properties. Calculate your allowable loss using Form 8582, then transfer it to Schedule E.

Part IV: Income or Loss From Real Estate Mortgage Investment Conduits (REMICs)

You must fill out Part IV if you have a residual interest in a real estate mortgage investment conduit (REMIC). A REMIC is a type of investment that pools mortgages and issues mortgage-backed securities.

As a REMIC investor, you’ll receive a quarterly statement called Schedule Q, which lists your share of the income and expenses. This document will help you enter the required details in Part IV of Schedule E.

If you’re the holder of a regular interest in a REMIC, report your income directly on Form 1040 instead of Schedule E.

If you have holdings in more than one REMIC, list them on another sheet in the same format as Part IV. Then, combine the totals (columns D and E) and enter the amount on line 39.

There’s no requirement to file Schedule Q when filing your tax return; however, you should still keep it for your records.

FAQ: How to file a Schedule E

The purpose of Schedule E is to report income or loss from rental properties. The IRS treats rental earnings as passive income, meaning that it requires little effort or active involvement on your part. If you rent out real estate and provide essential services like heat, water, and electricity, you’d use Schedule E to declare your income and expenses.

Schedule C is where you report earnings and expenses related to personal services provided to tenants, such as cleaning, food delivery, and security. The IRS classifies these activities as business since they require substantial time and effort.

Yes, you can still use Schedule E to report your rental income and expenses if you own more than one property. The form provides space to list up to three rental units. There’s also room to include up to four partnerships or S corporations. If you have more than three rental units, you can complete and attach as many additional Schedule E forms as needed.

Our final thoughts

If you earn rental income, you must disclose your earnings and expenses on Schedule E and submit the form with your primary tax return, Form 1040. Schedule E has four parts, which makes it look daunting. However, you only need to fill out the one that applies to your tax situation.

Make sure to gather all the relevant receipts, statements, and other necessary documents to help you complete the form ahead of time. If you need help, consult a tax expert to guide you or to complete the form on your behalf. Visit our financial management resources to learn more about preparing your taxes.

Learn more about Finance Management

Learn more about Finance Management

- Tax on Rental Income: A Guide for Canadian Landlords

- The Essential Rental Property Expense Sheet

- How to Calculate Depreciation on Rental Property in Canada (And How to Claim It)

- How to Calculate Rental Property Depreciation in the U.S.

- What Rental Income Expenses Can You Claim on Your Tax Return as a Landlord?

- Capital Improvements vs. Repairs: What to Know for Your Rental Property Taxes

- How to Fill Out a T776 Form (Tax on Rental Income)

- A Guide to Reporting Rental Income: How to File a Schedule E

- Can A Landlord Claim a Rental Loss from Unpaid Rent?

- How Tenants Can Claim Rent on Their Tax Return

- Part 1: Accounting for Rental Properties: Common mistakes and how to avoid them

- Part 2: Accounting for Rental Properties: When to hire a bookkeeper or accountant

- Mastering a Mortgage Renewal: A Guide to Financial Confidence (Calculators Included)

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in Canada?

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in the United States?

- How to Calculate Rent and Get the Best Rent Estimate