- Finance Management

- 8 Minute Read

How to Calculate Depreciation on Rental Property in Canada (And How to Claim It)

Updated on Jul 24, 2025

Written By:

Verified By:

Your rental isn’t going to stay in pristine shape forever. Over time, things will break down and suffer damage, resulting in your investment gradually losing value. This loss in value is your rental property depreciation, a significant and unavoidable cost you face as a landlord.

Luckily, the Canada Revenue Agency (CRA) allows you to claim capital cost allowance (CCA) on your rental income. This helps you recoup some of the money you spend on acquiring and improving your rental. Always consult a tax professional to understand what deductions make sense for your financial situation.

In this guide, we’ll explain rental property depreciation and the ins and outs of claiming CCA in Canada, including how much you can claim annually as a tax deduction and how to calculate it.

What is rental property depreciation?

Rental property depreciation is an accounting process where you deduct the value of your property and any improvements you made to it from your taxes. Instead of claiming the total cost of your rental’s purchase price (as well as any improvements) in a single year, you spread it over many years.

CCA is the tax deduction based on rental property depreciation. The CRA has strict rules that limit how much CCA you can claim each year on your tax return.

The cost of land and routine maintenance

There are two key points to know about rental property depreciation.

First, land is exempt from depreciation, as it doesn’t degrade. Only the building and its various structural components, like heating systems, electrical wiring, water pipes, are eligible for depreciation.

Second, routine repairs are considered as current costs. They don’t qualify as depreciable expenses since they don’t increase the property’s value or extend its lifespan. Some examples would be fixing a clogged toilet, patching up a small hole in a wall, or replacing a broken handle on a kitchen cabinet. You can deduct the entire cost of these activities in the year they’re performed.

Learn more about other expenses you can deduct as a landlord.

How to Claim Depreciation on Rental Property: How to Calculate CCA

Below are the steps to calculate and claim CCA on a residential rental property in Canada.

Step 1: Determine your adjusted cost base.

The adjusted cost base (ACB) is the total investment in your rental property. This may include capital costs, which are all the upfront expenses that go into obtaining and improving your rental.

You can depreciate the ACB over time and claim it as an expense on your taxes. Here’s what you can include in your ACB:

- The purchase price: This is the amount you paid to purchase the property. You only include the price of the building, as land isn’t a depreciable asset.

- Closing costs: These include various expenses related to buying the rental unit. Some examples of eligible closing costs include legal fees, utility installation charges, and land transfer taxes. Remember: only the portion related to the building, not the land, is depreciable.

- Additions and improvements: These are substantial expenditures you make to your rental. Some examples include adding new windows and replacing the roof shingles. The functional value of these investments must extend beyond one year. Otherwise, the full cost is tax-deductible as a current expense in the year incurred. Learn more about the difference between capital and current costs.

- Soft costs: These are expenses related to renovating or altering your property. An example is the interest paid on a loan to finance a kitchen renovation.

Here’s the formula to calculate your ACB:

![Adjusted cost base is underlined. Under that is an equation with $ Purchase price of the rental property − $ Value of the land +[$ Closing costs x (% of costs related to building x .01)] + Other capital costs.](https://www.singlekey.com/wp-content/uploads/2024/04/rental-property-depreciation-stat1b-1024x480.png)

And here’s an example of the ACB calculation:

- You bought a rental property for $400,000.

- The land is valued at $80,000.

- Your closing costs are $8,000 and 80% of those costs are related to the building.

- You invest $25,000 in improvements before listing it on the market.

The ACB for your rental property would therefore equal $351,400 ($400,000 – $80,000 + ($8,000 x 0.80) + $25,000). This is the amount that’s eligible for depreciation.

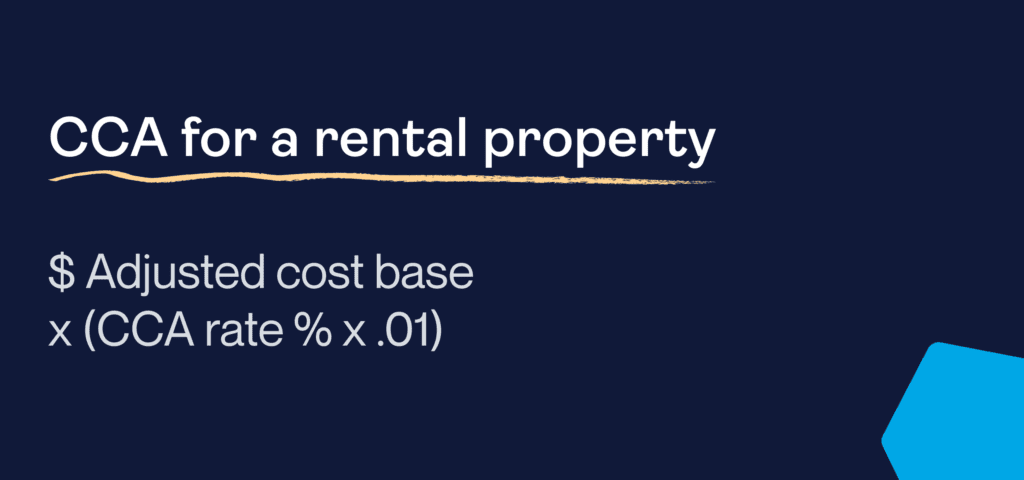

Step 2: Determine the CCA rate for your rental property

The next step is determining how much CCA you can legally deduct each year.

Under the CCA system, the CRA divides business assets into distinct classes. Each class has its own CCA rate, which defines the percentage of the asset’s value (adjusted cost base) you can claim as depreciation each year.

Most rental properties fall under Class 1, which includes all buildings acquired after 1987. You can add your property’s entire adjusted cost base in this class. The CCA rate for this class is 4%.

Step 3: Calculate the CCA to be claimed on your tax return

The final step is calculating the maximum CCA you can claim when filing your taxes. To do so, multiply your adjusted cost base by 4% (if your rental property is under Class 1). The resulting figure is the amount you can deduct from your rental income.

If we apply this calculation to our previous example, the allowable depreciation would be $14,056 ($351,400 x 0.04). Ordinarily, you’d be correct to claim this amount as an expense; however, since it’s the first year of operations for your rental, a quirk of the CCA system known as the half-year rule applies.

What is the half-year rule?

The half-year rule dictates that in the year you first acquire an asset, you can only claim half the depreciation you usually would. So, in the above scenario, you can only claim $7,028 worth of CCA against your rental income.

In the following years, the standard rules apply: you would apply the 4% CCA against your rental’s adjusted cost base as before.

However, before doing so, you must subtract the depreciation claimed in the prior year. Therefore, the balance eligible for the depreciation expense will decline yearly (unless you make new capital improvements to the property).

Under Canadian tax law, you cannot use depreciation to create or increase a rental loss—only to bring it down to zero.

Note: As of 2024, the half-year rule is being phased out (at least temporarily).

Latest updates to rental property depreciation guidance

In 2024, there were two important updates related to rental property depreciation:

Accelerated Capital Cost Allowance (ACCA)

The Canadian government introduced an ACCA to increase the maximum allowable depreciation rate from 4% to 10%. This applies to eligible new purpose-built rental housing. Learn more about ACCA here.

Depreciable Property Classes

Access to Classes 43.1 and 43.2 is now restricted for specific fossil-fuelled and low-efficiency waste-fuelled electrical generation equipment. Learn more about depreciable property classes here.

What are the benefits of rental property depreciation?

There are pros and cons to using the depreciation method and claiming CCA. On the plus side, the deduction can drastically slash your tax bill. You can apply depreciation against your rental profits for many years, allowing you to recover a sizable portion of the money you invest into your property.

You’re also not required to claim the maximum allowable CCA deduction in the current year it’s available. If you wish, you can use only a portion or defer the total amount to a future year when claiming it may be more advantageous (e.g., years where you earn a high rental income).

What are the drawbacks of rental property depreciation?

Despite the tax savings, there are some downsides when it comes to putting the rental property depreciation method in practice.

First, calculating depreciation can be tedious, especially if you own multiple rental properties and spend heavily on improvements. We’ve only scratched the surface regarding CCA rules and regulations—things can get more complex in practice.

Second, you may need to hire an accountant or other tax expert to help determine your CCA deductions and file your tax return. While doing so will give you peace of mind knowing the numbers reported to the CRA are likely correct, it’s another expense you must cover.

A third drawback of the rental property depreciation process is recaptured capital cost allowance. This one’s more complex because it only occurs if you decide to sell your property.

Let’s say you earn more from the sale of your rental than what’s remaining in your Class 1 asset balance (whatever you haven’t claimed as depreciation). In that case, the CRA will treat your gain as taxable income, which means you could face a steep tax bill.

Our final thoughts

It’s natural for your property to show wear and tear over time, making it necessary to invest in repairs and renovations. The good news is that you can obtain some financial relief during tax season by claiming CCA.

Understanding rental property depreciation and the rules for calculating CCA deductions can get complicated, so don’t hesitate to enlist a professional to help you—a qualified tax expert is always money well spent.

To learn more about managing your taxes for your rental property, visit our financial management resources.

Learn more about Finance Management

Learn more about Finance Management

- Tax on Rental Income: A Guide for Canadian Landlords

- The Essential Rental Property Expense Sheet

- How to Calculate Depreciation on Rental Property in Canada (And How to Claim It)

- How to Calculate Rental Property Depreciation in the U.S.

- What Rental Income Expenses Can You Claim on Your Tax Return as a Landlord?

- Capital Improvements vs. Repairs: What to Know for Your Rental Property Taxes

- How to Fill Out a T776 Form (Tax on Rental Income)

- A Guide to Reporting Rental Income: How to File a Schedule E

- Can A Landlord Claim a Rental Loss from Unpaid Rent?

- How Tenants Can Claim Rent on Their Tax Return

- Part 1: Accounting for Rental Properties: Common mistakes and how to avoid them

- Part 2: Accounting for Rental Properties: When to hire a bookkeeper or accountant

- Mastering a Mortgage Renewal: A Guide to Financial Confidence (Calculators Included)

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in Canada?

- How Do I Minimize Capital Gains Tax When Selling My Rental Property in the United States?

- How to Calculate Rent and Get the Best Rent Estimate