- Taxes

- 16 Minute Read

How to do a credit check on a tenant in Canada

Updated on Jun 8, 2026

Written By:

A tenant credit check helps landlords understand how an applicant has managed credit, debt and other financial obligations. In Canada, it's usually one part of a broader tenant screening process that may also include income verification, a background check, rental history and references.

To do a credit check on a tenant, landlords need to collect the applicant's basic identifying information and get written consent before pulling the report.

SingleKey's Tenant Report helps landlords look beyond the credit score by showing credit details alongside other screening information, such as income, employment, rental history and identity checks. That can make it easier to spot potential risk before approving a tenant.

At a glance

To run a tenant credit check, start with a rental application, get the applicant's written consent, choose the type of credit report you want to run and submit the applicant's details through a tenant screening platform. Once the report is ready, review it with the rest of the application, including income, employment, rental history and references.

Can landlords run a credit check on a tenant in Canada?

Yes. Landlords can run credit checks on potential tenants in Canada, but they must get the applicant's written consent before doing so. In addition, information collected during the credit check must comply with federal and provincial privacy laws, such as the Personal Information Protection and Electronic Documents Act (PIPEDA). That means a landlord cannot share an applicant's personal and credit information with unauthorized third parties.

The most common way to collect consent is through the rental application form. Include clear language explaining what information will be collected, why it is needed, how it may be used and which credit bureau or screening provider may be involved, where applicable. The applicant's signature provides a record of consent.

What information do you need to run a tenant credit check?

In most cases, landlords need a few basic details to run a credit check on a tenant. The minimum required information is:

- Full legal name

- Current address

- Date of birth

- Written consent from the applicant

These details help confirm the applicant's identity and return the correct credit report.

You may also collect a phone number, email address, employment information, proof of income, references and government-issued ID. These details are often more useful for the broader tenant screening process than for the credit check itself.

Be careful about requesting a social insurance number, or SIN. It is highly sensitive personal information and is not usually needed to run a tenant credit check, so landlords should avoid asking for it unless there is a clear reason and no reasonable alternative.

SingleKey's Tenant Report helps landlords collect and review key applicant information in one place, including an online rental application, credit report options, income and employment details, references and identity verification.

How to run a tenant credit check step by step

Here are the main steps to run a tenant credit check, from collecting the application to reviewing the report.

Collect a rental application

A rental application gives you the basic information you need to start the tenant screening process, including the credit check.

At a minimum, ask applicants to provide their full legal name, current address and date of birth. Employment information, proof of income, rental history, references and other details may not be required for the credit report itself, but they are useful for the broader screening process.

SingleKey's Tenant Report includes an online rental application, so applicants can submit key details in one place instead of sending paperwork back and forth.

While a credit report is important, do not approve or reject an applicant based on credit history alone. Review it alongside other factors, including income, employment stability, rent-to-income ratio, rental history and landlord references.

Get written consent

Do not pull an applicant's credit report without their permission. Landlords should get written consent before running a tenant credit check or sharing an applicant's personal information for screening.

The simplest way to collect consent is during the rental application process. The application should explain that a credit check may be used as part of tenant screening and that the applicant's permission is required before the check can be completed.

A digital application can make this step easier because the applicant can review the request, provide the required information and submit their consent online. This also gives landlords a clearer record of what was collected and when.

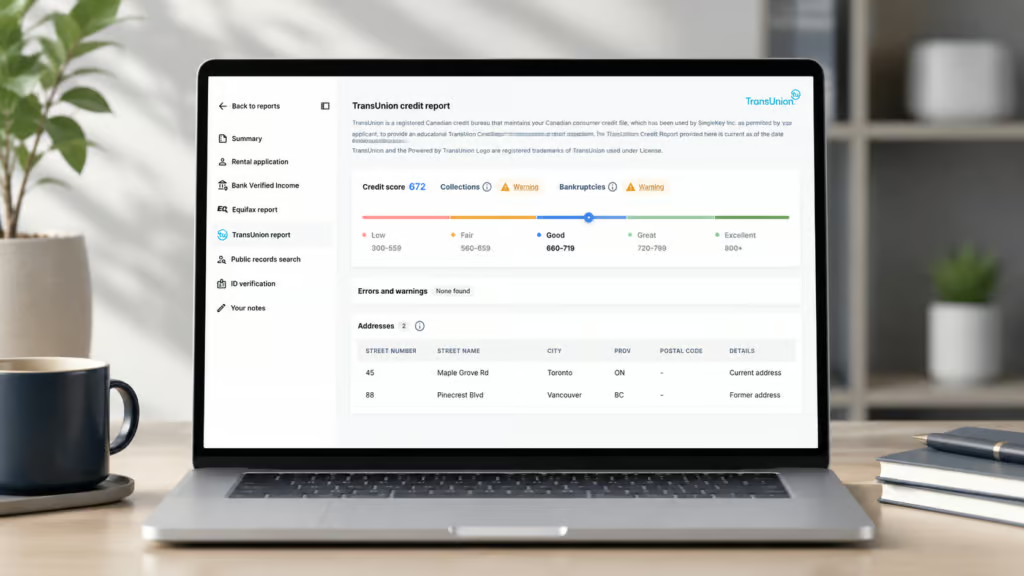

Choose an Equifax, TransUnion or Dual Credit Report

Once you have the applicant's details and written consent, choose the type of tenant credit report you want to run.

With SingleKey's Tenant Report, landlords can choose between an Equifax, TransUnion or Dual Credit Report. A single-bureau report may be enough in some cases, while a dual-bureau report can give you a broader view because credit bureaus may not always show the same information.

The credit check is included as part of the broader Tenant Report, so you can review credit information alongside other screening details instead of looking at the credit report in isolation. You can also learn more about Equifax vs. TransUnion before deciding which report is right for your screening process.

Invite the applicant or enter their details

After choosing the report type, you can move forward with the applicant's information.

Some landlords prefer to invite the applicant to complete the rental application online, provide consent and submit the details needed for the credit check. Others may already have the applicant's information and consent, and can enter those details directly.

SingleKey supports both paths. Landlords can send the applicant an invitation through the platform, or enter the applicant's information themselves if they already have the required details and consent. Once the request is submitted, the report is generated for review.

Review the tenant credit report

A tenant credit report can help you understand how an applicant has managed credit and debt over time. Some details worth reviewing include:

- Credit score

- Payment history

- Total outstanding debt

- Credit utilization

- Bankruptcies and consumer proposals

- Debts in collection

- Types of debt owed

- Liens and other court judgments

When reviewing a credit report, compare details such as address history with the applicant's rental application. If there are clear discrepancies, ask the applicant for clarification or review the file more closely before making a decision.

Avoid reviewing each section of the credit report in isolation. Use it to inform your decision, not to automatically approve or reject an applicant. A good tenant can still have a weaker credit history, especially if there is context behind it.

For example, a past bankruptcy does not always mean the applicant is unable to manage rent payments today. Since then, they may have secured a higher-paying job, built an emergency fund or reduced their debt.

Evaluate the credit report alongside the rest of the tenant screening file. Income, employment stability, rental history, landlord references and ID verification can all add important context before you make a final decision.

Want to review more than just credit history?

SingleKey's Tenant Report helps landlords look beyond the credit score by reviewing credit details alongside income, rental history, references and identity checks.

What should landlords look for in a tenant credit report?

The table below breaks down common tenant credit report details, what they mean and potential red flags to watch for during your review.

| Credit report item | What it shows | What to watch for |

|---|---|---|

| Credit score | A three-digit number that predicts how likely someone is to pay bills on time | A low score, which suggests an elevated risk of non-payment. Consider the broader report for context. |

| Payment history | A list of on-time, late and missed payments | A recent pattern of late or missed payments |

| Outstanding debts | The total amount owed for all loans and bills | High debt levels, especially when reviewed alongside the applicant's income |

| Accounts in collections | Unpaid debts sent to a collection agency | Significant debts in collections. Consider the age and size of the debt. |

| Bankruptcies and consumer proposals | Legal processes to eliminate or restructure debt that cannot be repaid | Active or recently completed bankruptcies and other negotiated settlements that may indicate ongoing financial distress |

| Credit inquiries, also called hard checks | Recent applications for new credit | A string of recent inquiries, which may signal a need for credit or other financial stress |

| Address history | Previous addresses on file | Address information that doesn't match what's in the rental application |

If you've never reviewed a credit report before, it can feel like a lot at first. Once you know what each section means, it becomes easier to spot patterns and review an applicant's credit history with more confidence.

With SingleKey's Tenant Report, landlords can review credit details alongside income, employment, rental history and other screening information, so the credit report is not being assessed on its own. You can also learn more about how to read and analyze a tenant credit report.

Should you accept a tenant-supplied credit report?

Landlords should avoid accepting credit reports directly from tenants because verifying their authenticity can be difficult. Tenant-supplied credit reports can be tampered with, outdated or incomplete, especially if shared as a PDF or screenshot.

If a tenant provides a credit report, check the date, source and details carefully. PDFs, screenshots and printouts can be altered or may not show the full report. If anything looks unusual or incomplete, ask for clarification or run the report through a trusted tenant screening provider.

SingleKey pulls credit data directly from Equifax and TransUnion during the screening process, reducing the risk of relying on an outdated or altered document. That gives landlords a clearer view of the applicant's current credit information instead of depending only on what the applicant chooses to share.

Run a tenant credit check with SingleKey

After collecting a rental application and written consent, landlords can run a tenant credit check through SingleKey's Tenant Report. The report shows credit details in a clean, easy-to-review format, including outstanding loans, hard inquiries, rent-to-income ratio and potential red flags such as court judgments or bankruptcies.

Beyond credit history, the Tenant Report can also include rental history, employment and income details, eviction history and ID verification. Reviewing these details together can help landlords make a more informed screening decision and reduce the risk of missed rent payments.

When it's time to screen the next applicant, SingleKey can help you run the credit check and review the broader tenant profile in one place.

Ready to screen your next applicant?

Start a Tenant Screening Report and review credit, income, references and identity in one place.

Frequently asked questions

Landlords usually start by collecting a rental application, getting written consent and submitting the applicant's details through a tenant screening provider or credit bureau. The credit report should then be reviewed with income, employment, rental history and references before making a decision.

Yes. Landlords should get clear written consent from the applicant before running a tenant credit check or sharing their personal information with a credit bureau or tenant screening provider. The applicant should understand what information is being collected, why it's needed and how it will be used.

Landlords usually need the applicant's full legal name, current address and date of birth, along with written consent. Some tenant screening providers may also ask for contact details or other information to help confirm the applicant's identity.

Yes. A Social Insurance Number is usually not required for tenant screening. In most cases, a full legal name, date of birth, current address and written consent are enough to run the check. Since a SIN is sensitive personal information, landlords should avoid asking for it unless there is a clear reason and no reasonable alternative.

Yes, but be careful. A credit report shared by the applicant as a PDF, screenshot or printout may be outdated, incomplete or difficult to verify. If you accept one, check the date, source and whether any key information appears to be missing. Using a verified tenant screening provider gives you a more reliable way to review credit information.

There isn't one credit score that automatically approves or rejects a rental applicant. Canadian credit scores generally range from 300 to 900, and a higher score usually suggests lower credit risk. Still, the score is only one part of the picture. Payment history, debt levels, income, rental history and references can all add useful context.

No. A credit check is useful, but you shouldn't rely on it alone. Review it alongside the full rental application, proof of income, employment details, rental history, references and any other screening information that helps you understand the applicant's overall profile.

Yes. SingleKey lets landlords choose between Equifax, TransUnion or both through a Dual Credit Report. This can give landlords a fuller view of an applicant's credit history, since the two credit bureaus may not always show the same information.

No. SingleKey uses a soft credit check for tenant screening, so it does not negatively affect the applicant's credit score. This can help reassure applicants who are worried about the screening process affecting their credit.

Related articles