Unlock insights and blogs to navigate property and tenant management successfully.

The fastest, most comprehensive tenant report—delivered instantly.

Unlock insights and blogs to navigate property and tenant management successfully.

The fastest, most comprehensive tenant report—delivered instantly.

Get credit and financial data from both credit bureaus to see the full picture

Easy, mobile friendly, and comprehensive online rental application form

We will contact your tenant’s references and share a recording and summary of the call

Search eviction court records from Openroom, CanLII, and SOQUIJ

AI-powered scan of income documents to detect signs of tampering or fraud

Confirm a tenant’s identity with AI-powered ID verification and liveness check

Unlock insights and blogs to navigate property and tenant management successfully.

Free Lease Agreement Forms for each province in one place

Conversations on real estate trends and property management strategies

Local tools and resources to help you manage your rental property successfully

Learn how to solve renting challenges from our experts

Articles on how to navigate the in-app SingleKey experience

A look at Canada’s average renter profile, affordability, and risk trends based SingleKey’s Q3 2025 rental applications

Get approved for any lease by showing landlords you’re a risk free tenant

Stand out from other applicants with the background check trusted by landlords

Affordable tenant insurance to protect renter's property and liability

Build your credit with every rent payment

The fastest, most comprehensive tenant report—delivered instantly.

Unlock insights and blogs to navigate property and tenant management successfully.

Free Lease Agreement Forms for each province in one place

Conversations on real estate trends and property management strategies

Local tools and resources to help you manage your rental property successfully

Learn how to solve renting challenges from our experts

Articles on how to navigate the in-app SingleKey experience

A look at Canada’s average renter profile, affordability, and risk trends based SingleKey’s Q3 2025 rental applications

Get approved for any lease by showing landlords you’re a risk free tenant

Stand out from other applicants with the background check trusted by landlords

Affordable tenant insurance to protect renter's property and liability

Build your credit with every rent payment

We analyzed hundreds of thousands of rental applications and data points across Canada to determine the average renter profile, affordability, and risk signals throughout Q3 2025.

Applicant Overview

32

2

27%

$2,063

$2,708

$67,536

$109,056

Full-time

72.5%

Part-time

6.4%

Student

5.2%

Self-employed

4.7%

Other

4.3%

Unemployed

3.6%

Retired/Pension

3.4%

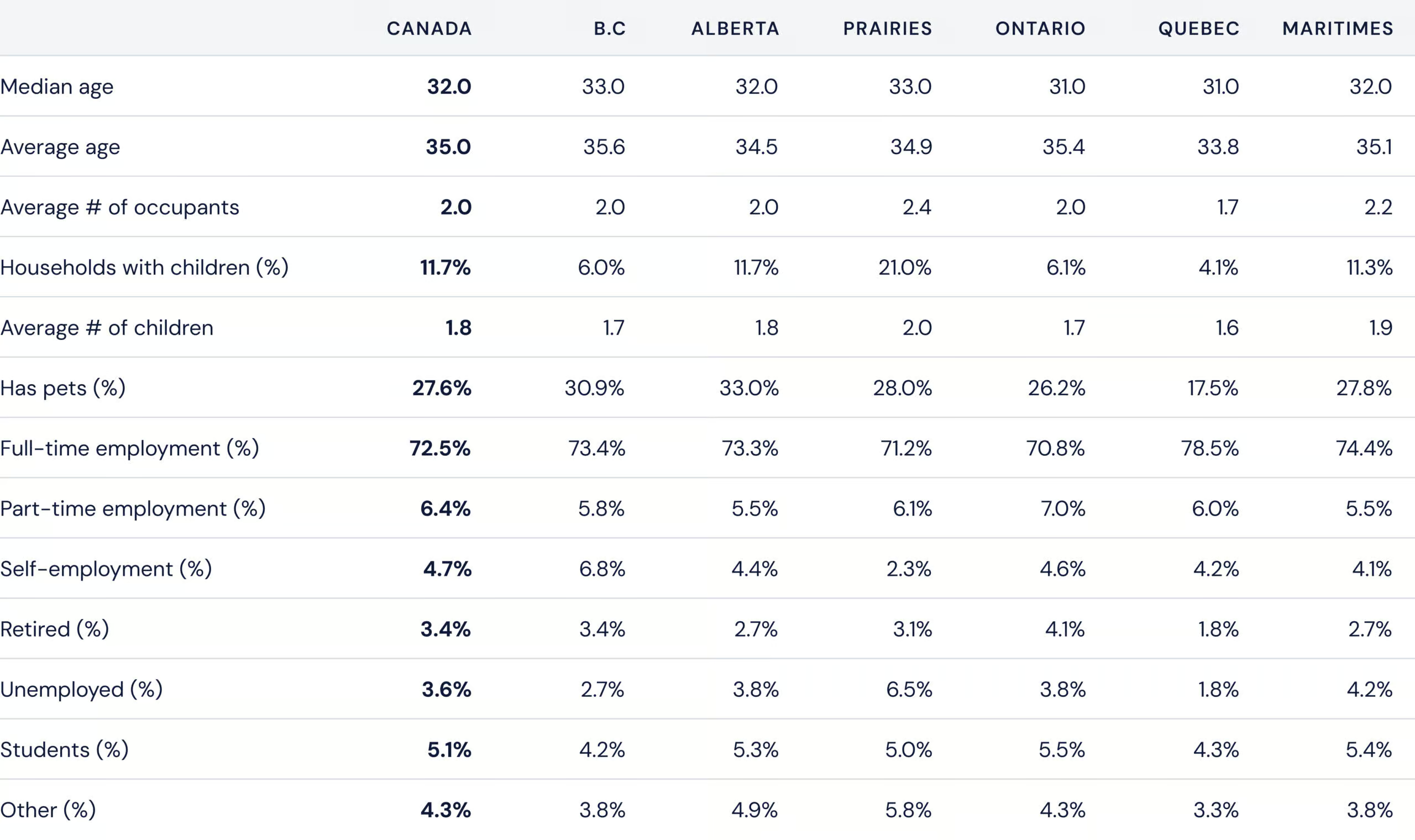

Canada’s renters have a median age of 32, are mostly full-time employed, and increasingly settled. About 12% have children and 28% have pets, reflecting a demographic renting later into life while starting families.

CANADA

CANADA

B.C

ALBERTA

PRAIRIES

ONTARIO

QUEBEC

MARITIMES

Median age

32.0

33.0

32.0

33.0

31.0

31.0

32.0

Average age

35.0

35.6

34.5

34.9

35.4

33.8

35.1

Average # of occupants

2.0

2.0

2.0

2.4

2.0

1.7

2.2

Has children (%)

11.7%

6.0%

11.7%

21.0%

6.1%

4.1%

11.3%

Average # of children

1.8

1.7

1.8

2.0

1.7

1.6

1.9

Has pets (%)

27.6%

30.9%

33.0%

28.0%

26.2%

17.5%

27.8%

Full-time employment (%)

72.5%

73.4%

73.3%

71.2%

70.8%

78.5%

74.4%

Part-time employment (%)

6.4%

5.8%

5.5%

6.1%

7.0%

6.0%

5.5%

Self-employment (%)

4.7%

6.8%

4.4%

2.3%

4.6%

4.2%

4.1%

Retired (%)

3.4%

3.4%

2.7%

3.1%

4.1%

1.8%

2.7%

Unemployed (%)

3.6%

2.7%

3.8%

6.5%

3.8%

1.8%

4.2%

Students (%)

5.1%

4.2%

5.3%

5.0%

5.5%

4.3%

5.4%

Other (%)

4.3%

3.8%

4.9%

5.8%

4.3%

3.3%

3.8%

CANADA

VANCOUVER

CALGARY

WINNIPEG

TORONTO

MONTREAL

HALIFAX

Median age

33.0

34.0

34.1

34

32.6

32.8

Average age

33.1

34.0

34.1

34.0

32.6

32.8

Average # of occupants

1.9

2.0

2.4

1.8

1.6

2.2

Has children (%)

6.1%

11.7%

21.4%

6.1%

4.1%

11.3%

Average # of children

1.6

1.7

2.0

1.4

1.6

1.9

Has pets (%)

22.1%

28.2%

24.4%

15.2%

12.7%

17.6%

Full-time employment (%)

72.8%

76.3%

70.3%

73.7%

79.0%

75.9%

Part-time employment (%)

7.0%

5.4%

6.6%

5.4%

6.8%

6.2%

Self-employment (%)

6.5%

5.1%

1.7%

5.9%

3.7%

5.1%

Retired (%)

1.3%

2.0%

2.6%

2.4%

1.5%

1.5%

Unemployed (%)

3.4%

3.2%

7.4%

3.2%

1.5%

3.3%

Students (%)

7.8%

4.7%

3.5%

7.1%

5.7%

6.9%

Other (%)

1.0%

3.4%

7.9%

2.3%

1.8%

1.1%

CANADA

CANADA

B.C

ALBERTA

PRAIRIES

ONTARIO

QUEBEC

MARITIMES

Rent price ($)

$2,063

$2,490

$1,869

$1,683

$2,159

$1,623

$1,890

Household income ($)

$109,057

$125,516

$108,248

$91,058

$110,800

$89,522

$98,765

Personal income ($)

$67,537

$78,033

$68,057

$52,705

$67,410

$59,895

$61,672

Rent-to-income (%)

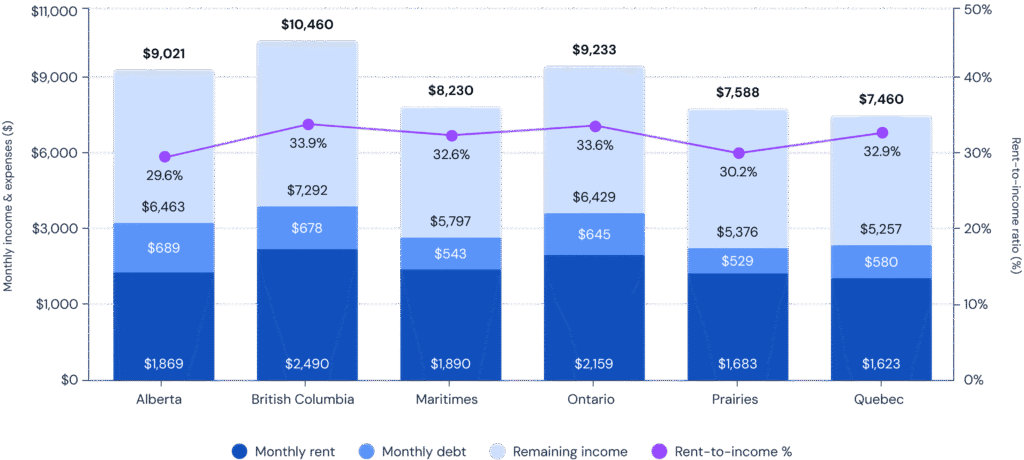

32.6%

33.9%

29.6%

30.2%

33.6%

32.9%

32.6%

Monthly debt payments ($)

$645

$678

$689

$529

$645

$579

$544

Rent + debt-to-income (%)

38.6%

40.0%

36.5%

35.3%

39.2%

39.4%

38.5%

CANADA

VANCOUVER

CALGARY

WINNIPEG

TORONTO

MONTREAL

HALIFAX

Rent price ($)

$2,891

$2,028

$1,713

$2,581

$1,605

$2,145

Household income ($)

$146,194

$116,390

$107,703

$142,346

$89,748

$112,449

Personal income ($)

$92,721

$77,224

$63,526

$94,370

$61,506

$71,539

Rent-to-income (%)

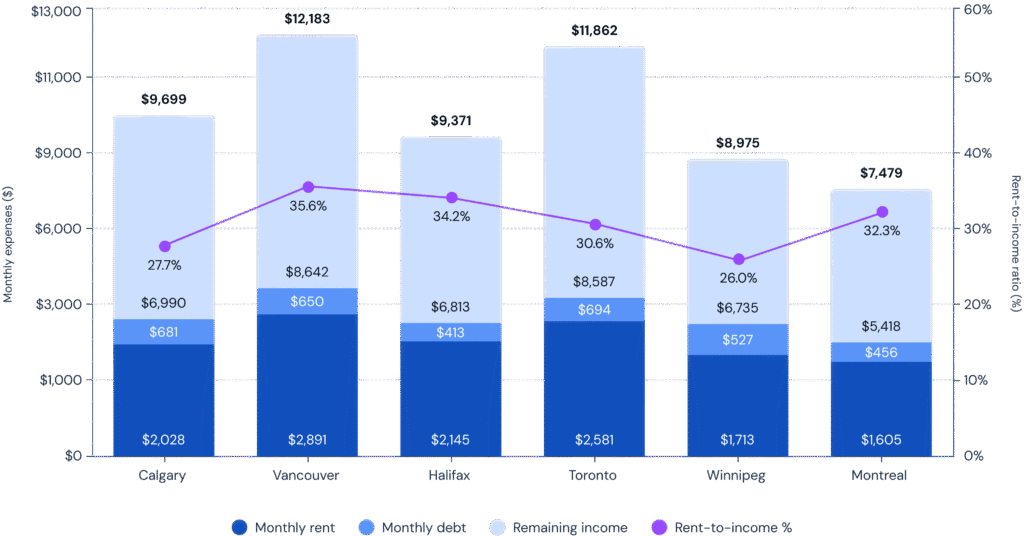

35.6%

27.7%

26.0%

30.6%

32.3%

34.2%

Monthly debt payments ($)

$650

$681

$526

$693

$456

$413

Rent + debt-to-income (%)

41.6%

33.4%

31.0%

34.2%

37.3%

37.4%

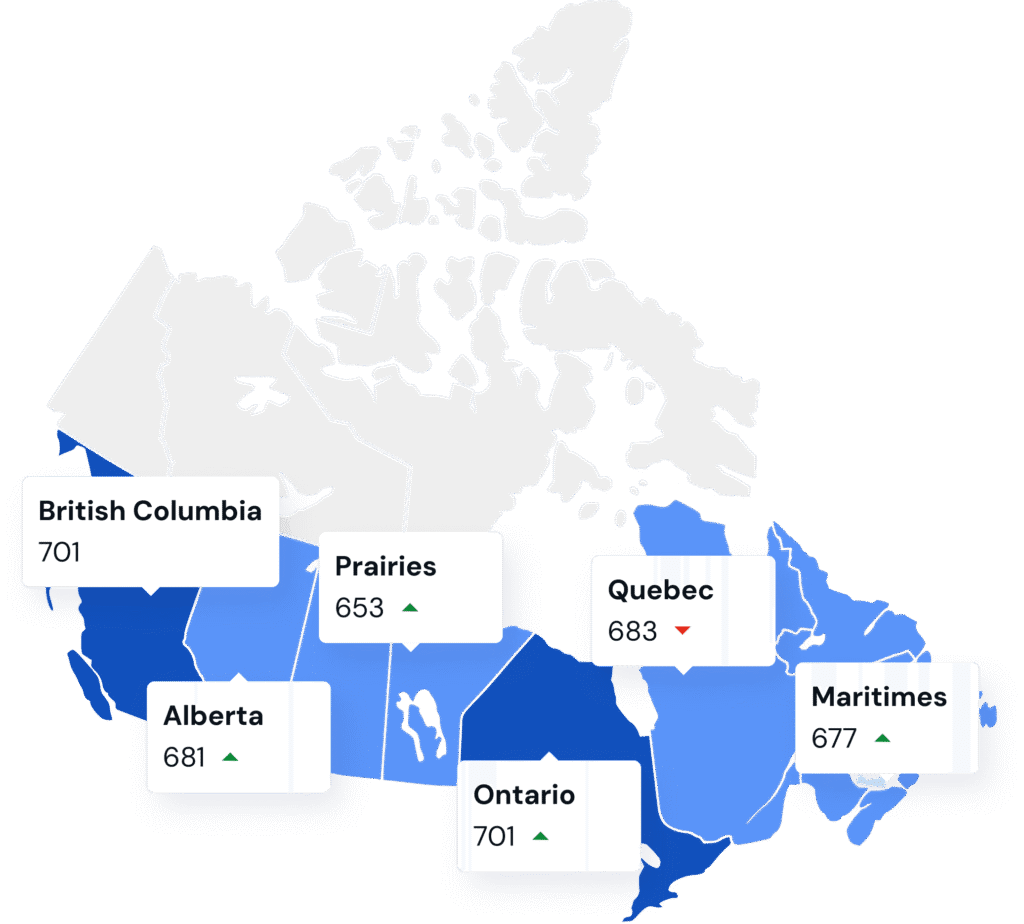

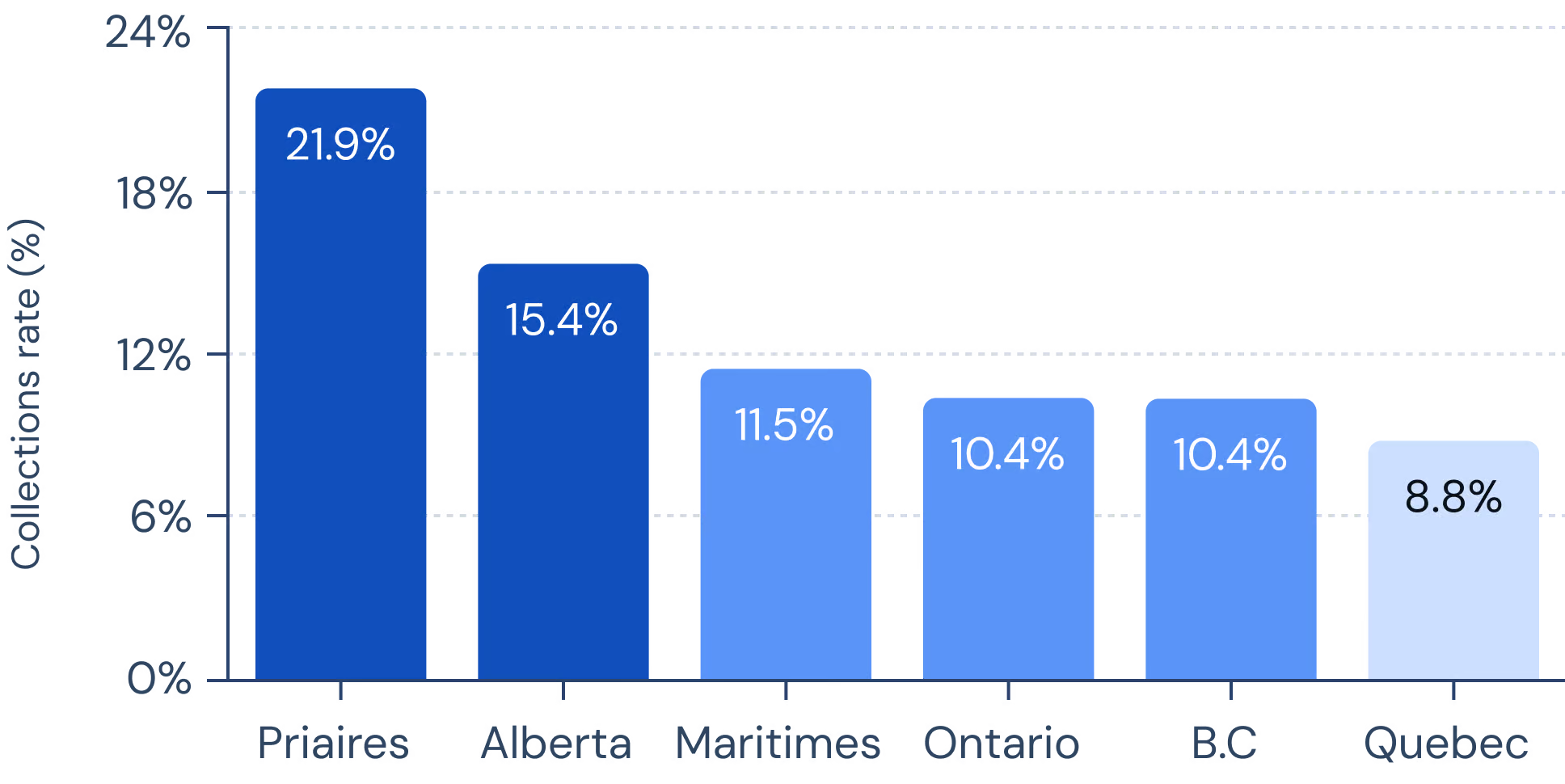

Rent is more affordable in central Canada, however these renters have higher collection rates, bankruptcies, and lower credit scores, indicating higher financial instability.

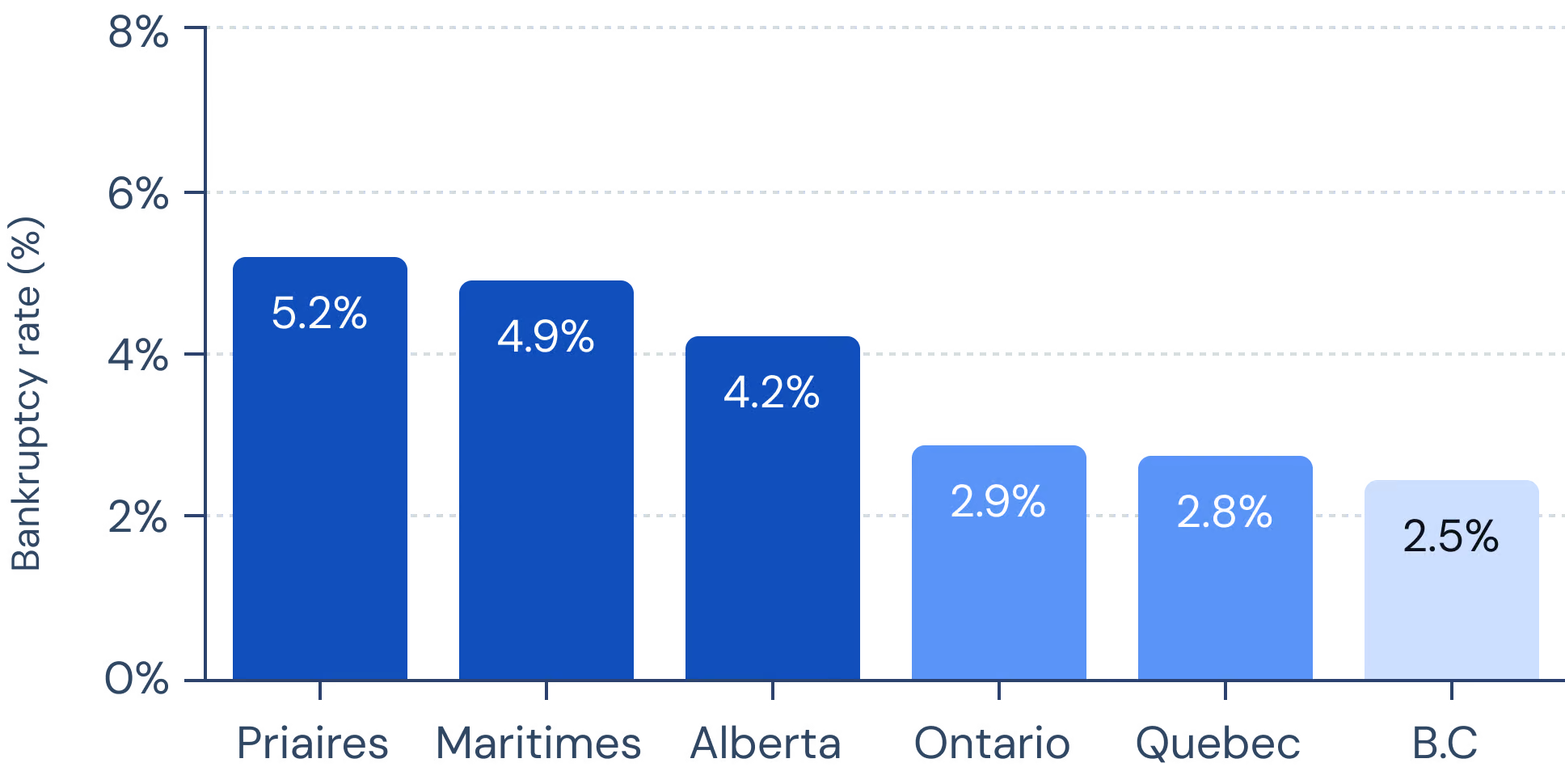

CANADA

CANADA

B.C

ALBERTA

PRAIRIES

ONTARIO

QUEBEC

MARITIMES

Credit score

693

702

682

653

701

683

677

Rent-to-income (%)

32.6%

33.9%

29.6%

30.2%

33.6%

32.9%

32.6%

Debt-to-income (%)

7.9%

7.6%

9.0%

7.1%

7.6%

8.3%

6.7%

Bankruptcies (%)

3.3%

2.5%

4.2%

5.2%

2.9%

2.8%

4.9%

Collections (%)

11.6%

10.4%

15.4%

21.9%

10.4%

8.8%

11.5%

Application declined (%)

18.0%

25.2%

14.7%

18.3%

17.7%

21.7%

16.7%

CANADA

VANCOUVER

CALGARY

WINNIPEG

TORONTO

MONTREAL

HALIFAX

Credit score

731

703

655

735

688

705

Rent-to-income (%)

35.6%

27.7%

26.0%

30.6%

32.3%

34.2%

Debt-to-income (%)

7.2%

7.8%

6.7%

5.7%

6.4%

4.1%

Bankruptcies (%)

2.1%

2.9%

3.9%

1.1%

2.1%

1.7%

Collections (%)

7.3%

10.1%

18.9%

4.3%

7.7%

6.7%

Application declined (%)

13.8%

9.5%

31.3%

13.5%

14.4%

5.0%

In Winnipeg, 21.4% of renters have children, and the city’s renters have the oldest median age in Canada (34.1). This indicates that Winnipeg offers greater affordability for renters seeking to start families.

The traditional model of "rent in 20s, buy before kids" is breaking down - renters are now in their mid-30s, and whether they have families depends more on regional affordability than age.

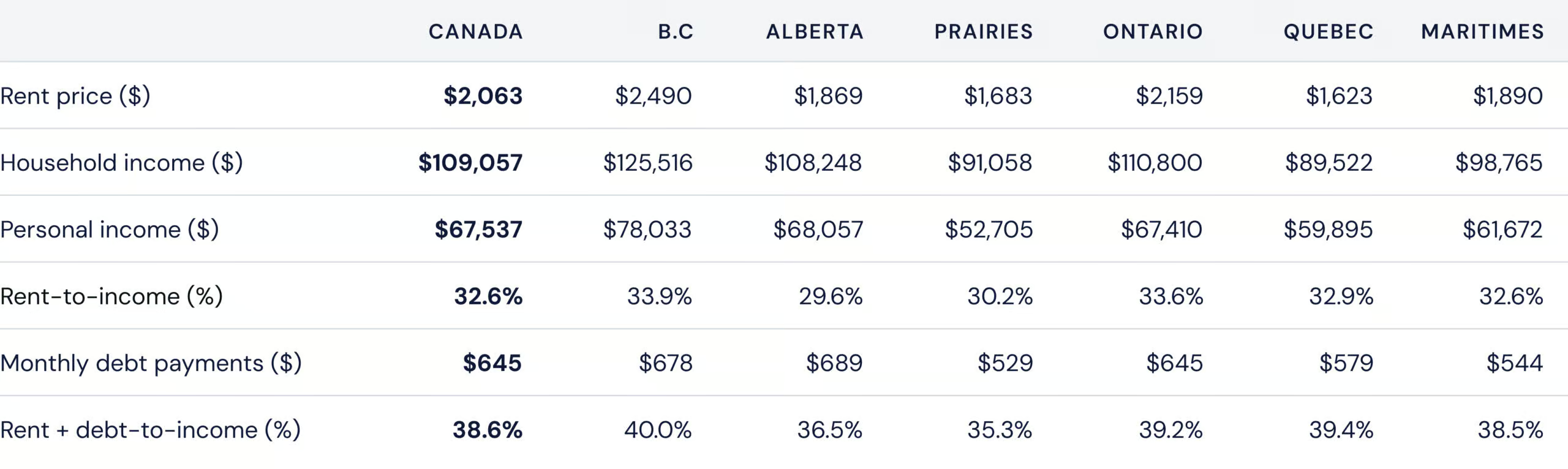

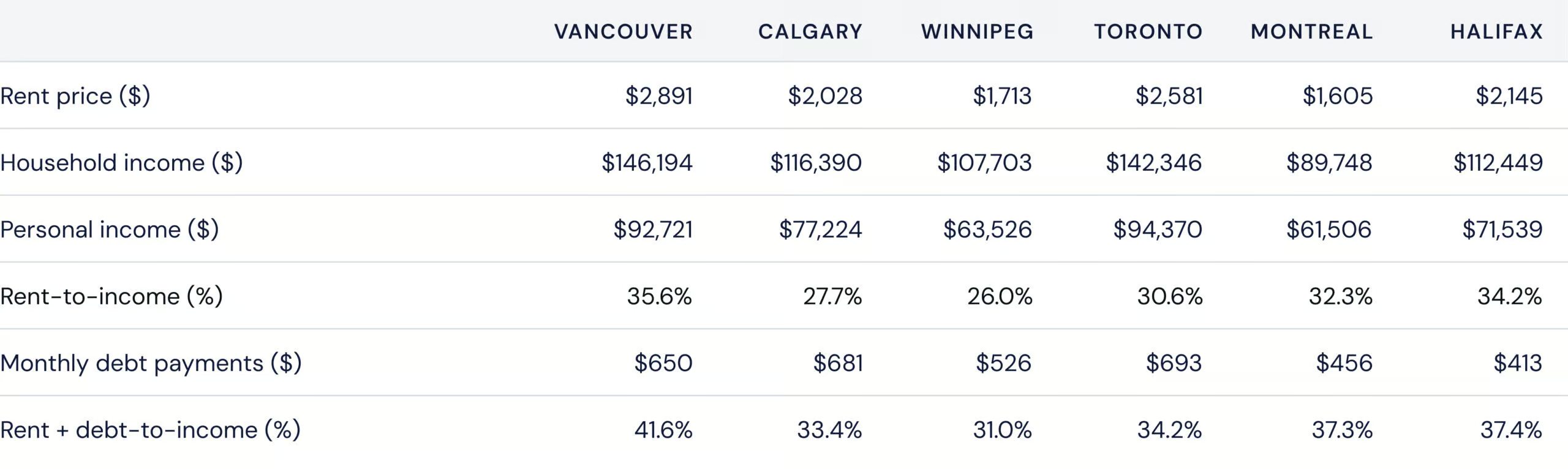

Rents are exceeding 30% of gross income across most of the country. Currently, Halifax and Montreal tenants face the most affordability strain, seeing lower incomes yet higher rent prices on average. Toronto and Vancouver appear less affordable overall, yet renters have higher incomes on average, which offsets higher rent costs.

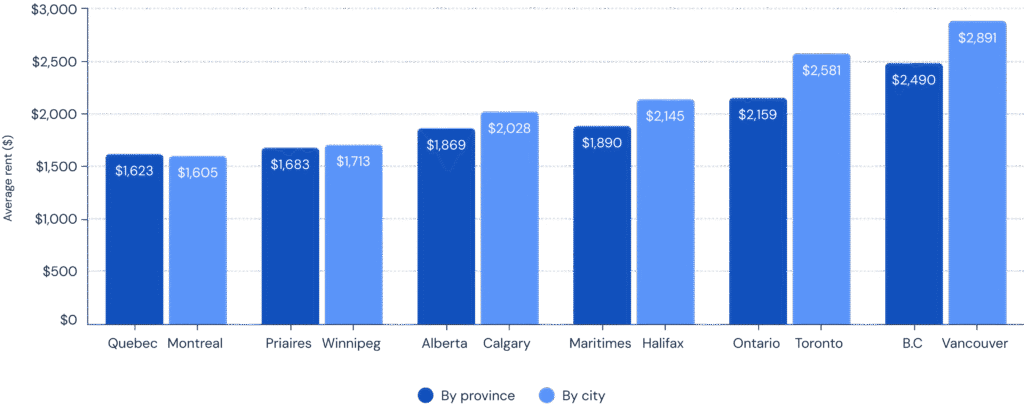

Vancouver and Toronto continue to lead as Canada’s most expensive rental markets, while Quebec and the Prairies remain the last bastions of relative affordability.

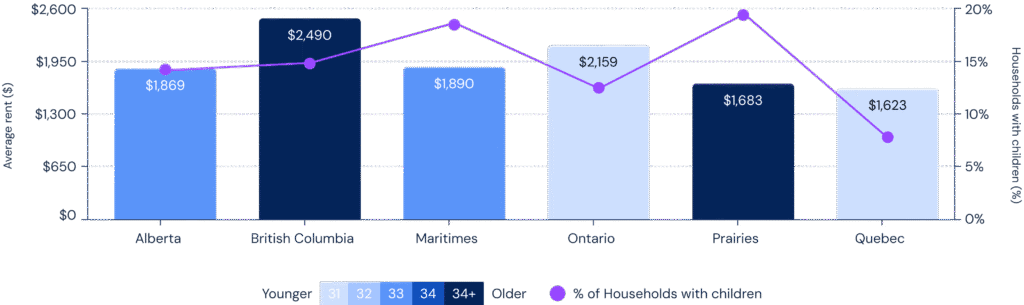

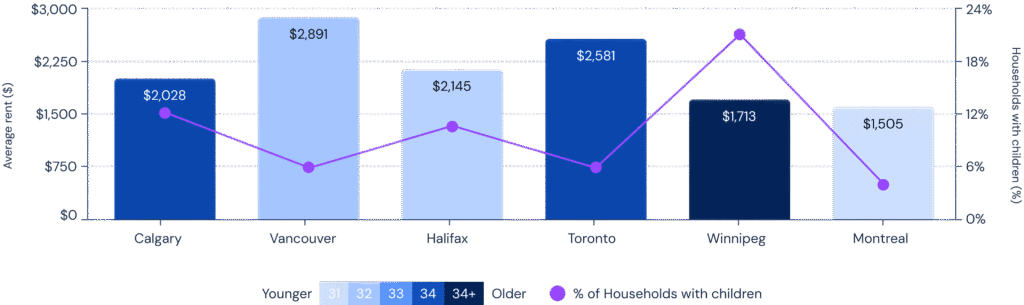

Higher rents tend to coincide with older renter populations, while provinces with lower rents (like the Prairies and Quebec) see a higher share of households with children.

How to read this chart: Bars show average rent by age group, with darker shades for older renters. The purple line represents the share of households with children, showing where family renters are most concentrated.

Despite regional income differences, renters across Canada face similar affordability pressures. Rent consumes about one-third of household income, and when combined with debt, many households are left with limited disposable income.

By province

How to read this chart: The bar chart shows monthly expenses of rent, debt, and a renter’s income after these expenses are subtracted. The top line number shows the monthly gross household income before taxes. The purple line tracks the rent-to-income ratio, highlighting where housing costs take up more of renters’ pay.

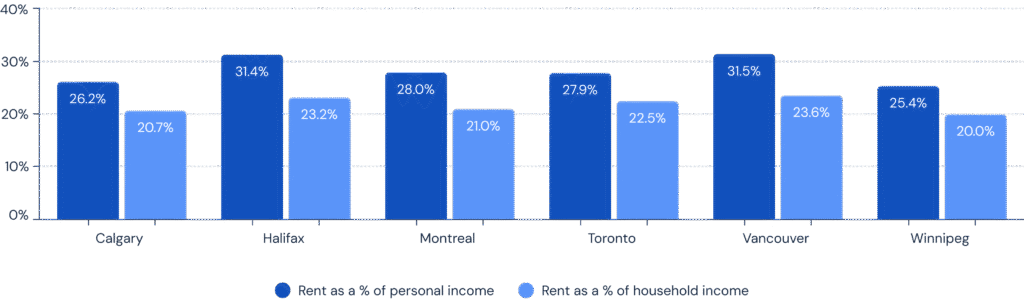

Affordability improves in dual-income households: rent’s share drops by nearly eight points when measured against household rather than personal income, allowing these renters to better absorb high rental costs.

How to read this chart: Each city shows rent as a share of personal income and household income. The gap between the two reflects how renting is more affordable on two incomes instead of one. All income is measured as gross monthly income before taxes.

While over half (53%) of renters earn under $60,000 annually, an increasing share fall into higher income brackets — with many earning well above $100,000. This shift points to a more affluent renter base overall, even as rent continues to consume roughly one-third of household income.

$67,536

$109,056

28.4%

25.1%

19.2%

10.7%

8.1%

3.1%

5.5%

Province

AVG RENT

MONTHLY INCOME

RTI

British Columbia

$2,490

$10,460

33.9%

Alberta

$1,869

$9,021

29.6%

Prairies

$1,683

$7,588

30.2%

Ontario

$2,159

$9,233

33.6%

Quebec

$1,623

$7,460

32.9%

Maritimes

$1,890

$8,230

32.6%

Province

AVG RENT

MONTHLY INCOME

RTI

Vancouver

$2,891

$12,183

35.6%

Calgary

$2,028

$9,699

27.7%

Winnipeg

$1,713

$8,975

26.0%

Toronto

$2,581

$11,862

30.6%

Montreal

$1,605

$7,479

32.3%

Halifax

$2,145

$9,371

34.2%

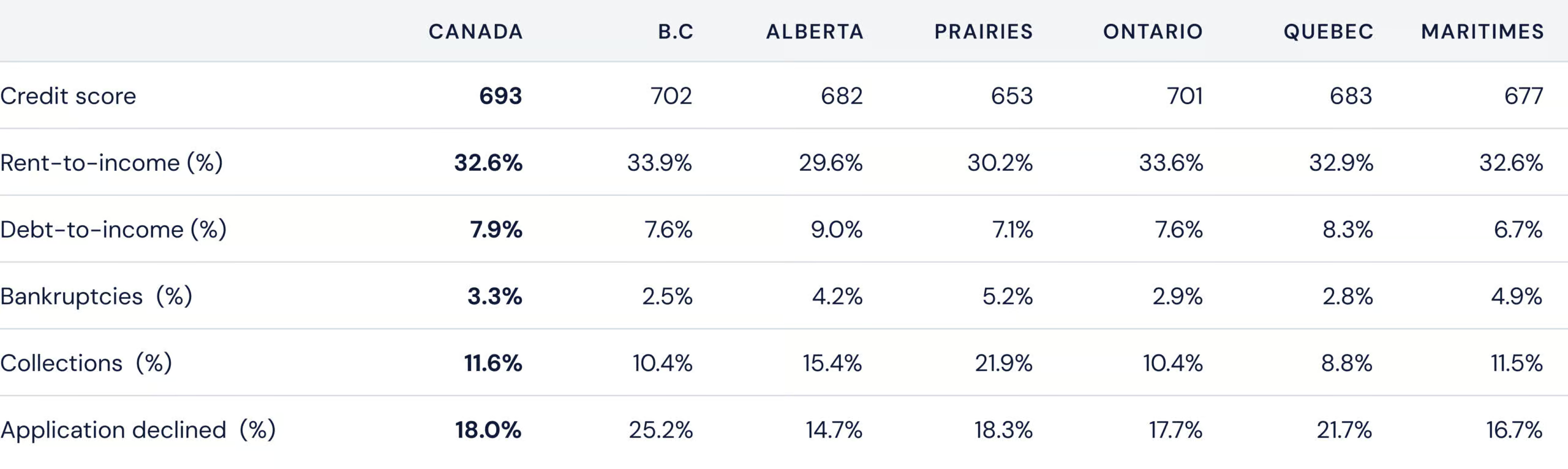

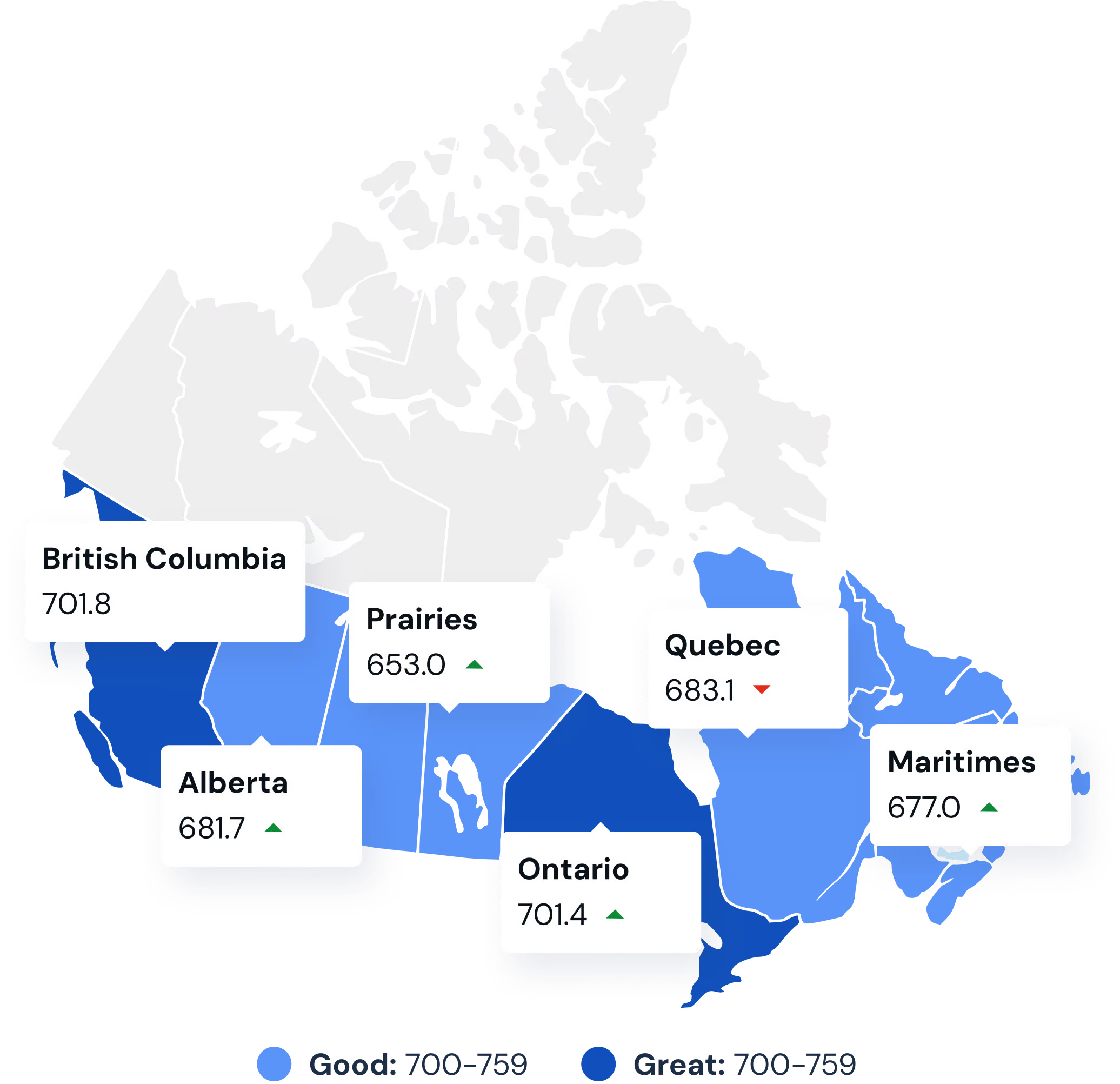

On average, renters fall in the good credit range, with a large share in great to excellent. Year over year, we are seeing credit strength improve over time across the provinces, while this trend is reversed in larger cities. Metropolitan renters tend to have better credit suggesting more financially stable renters, compared to rural counterparts. Selecting tenants with proven credit discipline, requiring co-signers, or rent guarantees for weaker profiles can reduce delinquency risk.

693.4

RANK

CREDIT SCORE RANGE

SEGMENT SIZE

Low

360-559

12.3%

Fair

560-639

14.2%

Good

640-699

20.5%

Great

700-759

24.6%

Excellent

760+

28.4%

city

CREDIT SCORe

yoy

Vancouver

731.1

Calgary

702.8

Winnipeg

654.8

Toronto

732.7

Montreal

688.2

Halifax

705.4

Canada has a favourable rental environment for property owners. Stronger tenant credit health means fewer payment issues, better tenant quality, less turnover, greater retention, and greater financial stability across rental portfolios.

Credit disparities by region suggest landlords in Winnipeg or the Prairies should tighten screening, personalize terms, and maintain financial buffers to offset higher tenant-risk variability.

This could indicate growing financial strain among residents despite high income levels, possibly tied to increased debt loads or cost-of-living pressures. If this trend continues, it may signal emerging credit risk in an otherwise financially stable market.

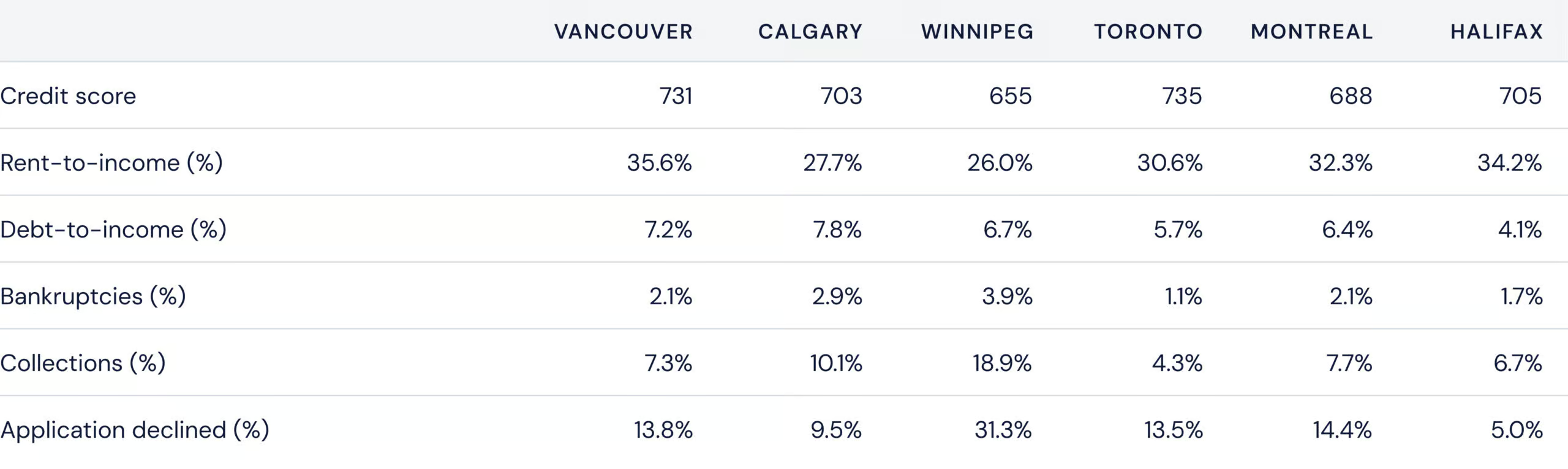

Although metropolitan cities are more expensive for tenants to afford, we see better quality tenants cluster within them across risk indicators such as collections rates, bankruptcy rates, and average credit scores. Property investors looking to expand their portfolios of income properties should plan strategically. Property prices may be lower in more rural areas, but tenant financial stability and risk increases in those areas as well.

18.9%

3.9%

655

10.1%

2.9%

703

7.7%

2.1%

688

7.3%

2.1%

731

6.7%

1.7%

705

4.3%

1.1%

735

With the lowest delinquency and bankruptcy rates, and maintaining strong credit performance, these cities represent lower payment risk and higher tenant reliability, making them strong rental market opportunities for landlords.

Calgary’s rates indicate higher-than-average debt strain despite relatively solid credit scores, while Montreal’s slightly lower scores and moderate collections suggest income-to-debt imbalances among renters.

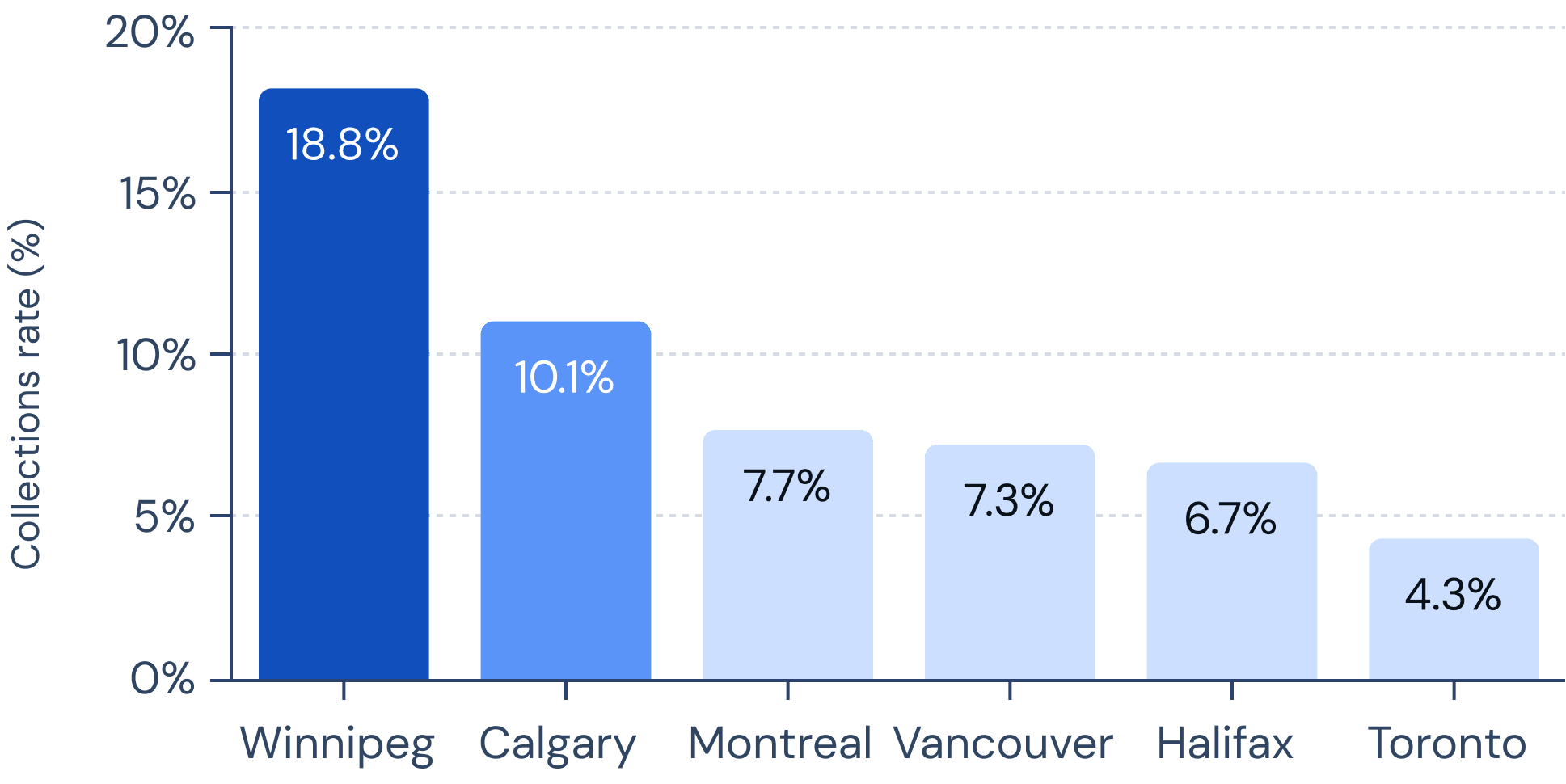

Nearly 1 in 5 tenants have accounts in collections and the highest bankruptcy rate among major cities. These trends, coupled with the city’s lower average credit score, suggest significant financial stress and a higher likelihood of missed or late rent payments.

We analyzed hundreds of thousands of rental applications and data points across Canada to determine the average renter profile, affordability, and risk signals throughout Q3 2025.

Median age

32

Average # of occupants

2

Households with pets

27%

Households with children

20%

Average monthly rent

$2,063

Monthly debt + rent payments

$2,708

Average personal income

$67,536

Average household income

$109,056

EMPLOYMENT TYPE

SEGMENT SIZE

Full-time

72.5%

Part-time

6.4%

Student

5.2%

Self-employed

4.7%

Other

4.3%

Unemployed

3.6%

Retired/Pension

3.4%

Canada’s renters have a median age of 33, are mostly full-time employed, and increasingly settled. About 12% have children and 28% have pets, reflecting a demographic renting later into life while starting families.

The average Canadian renter earns a personal income of $67K and a household income of $109K, yet faces rising costs. Rent alone consumes about one-third of earnings and total debt payments pushing overall financial strain near 40% of income.

Rent is more affordable in central Canada, however these renters have higher collection rates, bankruptcies, and lower credit scores, indicating higher financial instability.

Higher rent cost areas (Vancouver and Toronto) are less affordable, have fewer families as renters, and are young professional hubs. Lower rent cost areas (Winnipeg, Maritimes, Prairies) are more affordable and family-friendly. However, across the board renters are left with less than half of their pre-tax gross income to pay for bills, taxes, and cost of living, outside of their rent. This makes saving earnings difficult month to month. Renter demographics are aging. Renters are staying longer in their rentals and building families in them, further illuminating the unaffordable nature of home ownership across the country.

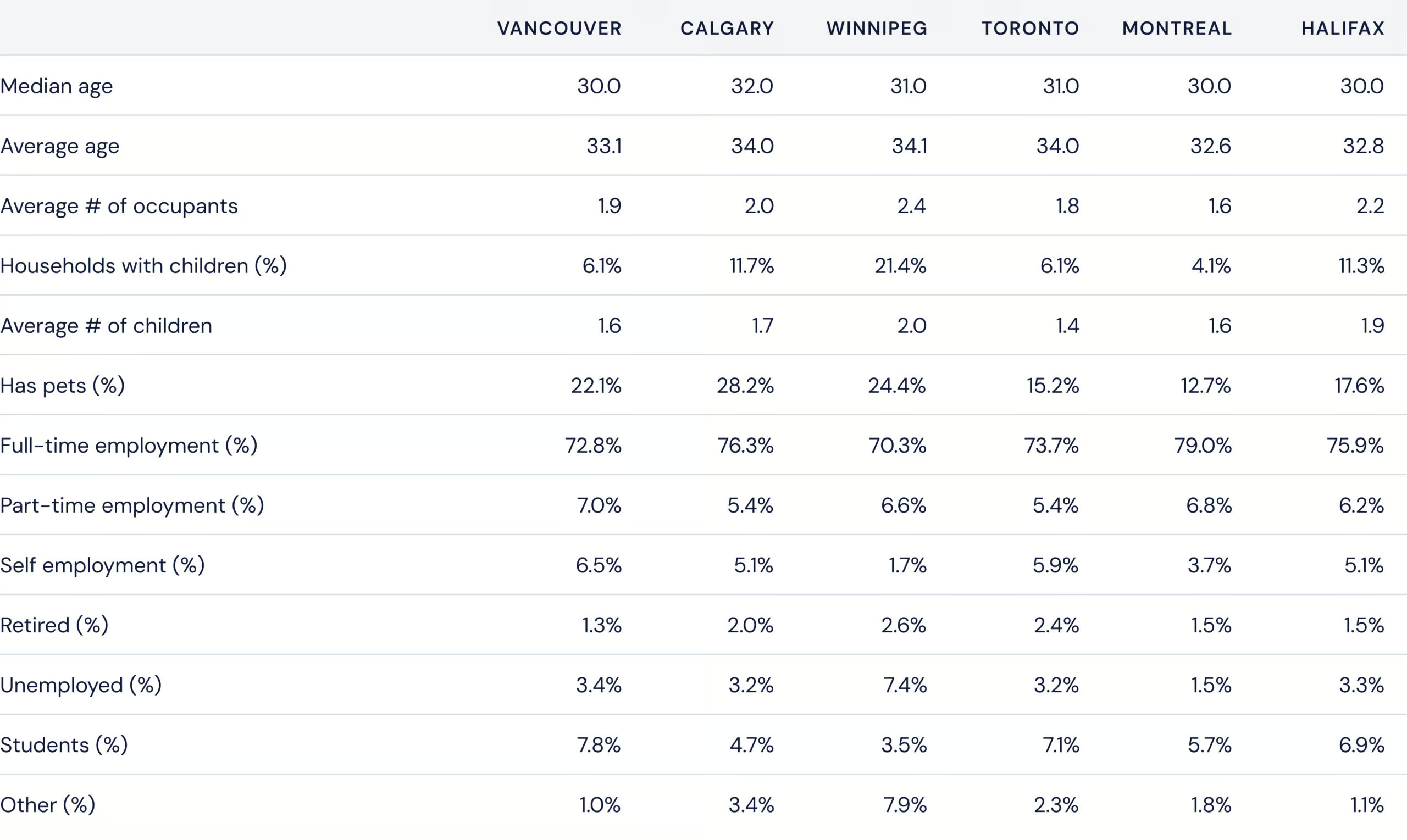

In Winnipeg, 21.4% of renters have children, and the city’s renters have the oldest median age in Canada (34.1). This indicates that Winnipeg offers greater affordability for renters seeking to start families.

The traditional model of "rent in 20s, buy before kids" is breaking down - renters are now in their mid-30s, and whether they have families depends more on regional affordability than age.

Rents are exceeding 30% of gross income across most of the country. Currently, Halifax and Montreal tenants face the most affordability strain, seeing lower incomes yet higher rent prices on average. Toronto and Vancouver appear less affordable overall, yet renters have higher incomes on average, which offsets higher rent costs.

Vancouver and Toronto continue to lead as Canada’s most expensive rental markets, while Quebec and the Prairies remain the last bastions of relative affordability.

Higher rents tend to coincide with older renter populations, while provinces with lower rents (like the Prairies and Quebec) see a higher share of households with children.

How to read this chart: The bar chart shows monthly expenses of rent, debt, and a renter’s income after these expenses are subtracted. The top line number shows the monthly gross household income before taxes. The purple line tracks the rent-to-income ratio, highlighting where housing costs take up more of renters’ pay.

Despite regional income differences, renters across Canada face similar affordability pressures. Rent consumes about one-third of household income, and when combined with debt, many households are left with limited disposable income.

How to read this chart: Bars show average rent by age group, with darker shades for older renters. The purple line represents the share of households with children, showing where family renters are most concentrated.

Affordability improves in dual-income households: rent’s share drops by nearly eight points when measured against household rather than personal income, allowing these renters to better absorb high rental costs.

How to read this chart: Each city shows rent as a share of personal income and household income. The gap between the two reflects how renting is more affordable on two incomes instead of one. All income is measured as gross monthly income before taxes.

While over half (53%) of renters earn under $60,000 annually, an increasing share fall into higher income brackets — with many earning well above $100,000. This shift points to a more affluent renter base overall, even as rent continues to consume roughly one-third of household income.

$67,536

$109,056

PERSONAL INCOME

RANGE

SEGMENT SIZE

28.4%

25.1%

19.2%

10.7%

8.1%

3.1%

5.5%

Province

AVG

RENT

MONTHLY INCOME

RTI

B.C

$2,490

$10,460

33.9%

Alberta

$1,869

$9,021

29.6%

Prairies

$1,683

$7,588

30.2%

Ontario

$2,159

$9,233

33.6%

Quebec

$1,623

$7,460

32.9%

Maritimes

$1,890

$8,230

32.6%

CITY

AVG

RENT

MONTHLY INCOME

RTI

Vancouver

$2,891

$12,183

35.6%

Calgary

$2,028

$9,699

27.7%

Winnipeg

$1,713

$8,975

26.0%

Toronto

$2,581

$11,862

30.6%

Montreal

$1,605

$7,479

32.3%

Halifax

$2,145

$9,371

34.2%

On average, renters fall in the good credit range, with a large share in great to excellent. Year over year, we are seeing credit strength improve over time across the provinces, while this trend is reversed in larger cities. Metropolitan renters tend to have better credit suggesting more financially stable renters, compared to rural counterparts. Selecting tenants with proven credit discipline, requiring co-signers, or rent guarantees for weaker profiles can reduce delinquency risk.

693.4

RANK

CREDIT SCORE RANGE

SEGMENT

SIZE

Low

360-559

12.3%

Fair

560-639

14.2%

Good

640-699

20.5%

Great

700-759

24.6%

Excellent

760+

28.4%

city

CREDIT SCORe

yoy

Vancouver

731.1

Calgary

702.8

Winnipeg

654.8

Toronto

732.7

Montreal

688.2

Halifax

705.4

Canada has a favourable rental environment for property owners. Stronger tenant credit health means fewer payment issues, better tenant quality, less turnover, greater retention, and greater financial stability across rental portfolios.

Credit disparities by region suggest landlords in Winnipeg or the Prairies should tighten screening, personalize terms, and maintain financial buffers to offset higher tenant-risk variability.

This could indicate growing financial strain among residents despite high income levels, possibly tied to increased debt loads or cost-of-living pressures. If this trend continues, it may signal emerging credit risk in an otherwise financially stable market.

Although metropolitan cities are more expensive for tenants to afford, we see better quality tenants cluster within them across risk indicators such as collections rates, bankruptcy rates, and average credit scores. Property investors looking to expand their portfolios of income properties should plan strategically. Property prices may be lower in more rural areas, but tenant financial stability and risk increases in those areas as well.

Collections

18.9%

Bankruptcies

3.9%

Credit score

655

Collections

10.1%

Bankruptcies

2.9%

Credit score

703

Collections

7.7%

Bankruptcies

2.1%

Credit score

688

Collections

7.3%

Bankruptcies

2.1%

Credit score

731

Collections

6.7%

Bankruptcies

1.7%

Credit score

705

Collections

4.3%

Bankruptcies

1.1%

Credit score

735

With the lowest delinquency and bankruptcy rates, and maintaining strong credit performance, these cities represent lower payment risk and higher tenant reliability, making them strong rental market opportunities for landlords.

Calgary’s rates indicate higher-than-average debt strain despite relatively solid credit scores, while Montreal’s slightly lower scores and moderate collections suggest income-to-debt imbalances among renters.

Nearly 1 in 5 tenants have accounts in collections and the highest bankruptcy rate among major cities. These trends, coupled with the city’s lower average credit score, suggest significant financial stress and a higher likelihood of missed or late rent payments.

We analyzed hundreds of thousands of rental applications and data points across Canada to determine the average renter profile, affordability, and risk signals throughout Q3 2025.

Median age

32

Average # of occupants

2

Households with pets

27%

Households with children

20%

Average monthly rent

$2,063

Monthly debt + rent payments

$2,708

Average personal income

$67,536

Average household income

$109,056

EMPLOYMENT

TYPE

SEGMENT

SIZE

Full-time

72.5%

Part-time

6.4%

Student

5.2%

Full-time

72.5%

Self-employed

4.7%

Other

4.3%

Unemployed

3.6%

Retired/Pension

3.4%

Canada’s renters have a median age of 32, are mostly full-time employed, and increasingly settled. About 12% have children and 28% have pets, reflecting a demographic renting later into life while starting families.

The average Canadian renter earns a personal income of $67K and a household income of $109K, yet faces rising costs. Rent alone consumes about one-third of earnings and total debt payments pushing overall financial strain near 40% of income.

Rent is more affordable in central Canada, however these renters have higher collection rates, bankruptcies, and lower credit scores, indicating higher financial instability.

Higher rent cost areas (Vancouver and Toronto) are less affordable, have fewer families as renters, and are young professional hubs. Lower rent cost areas (Winnipeg, Maritimes, Prairies) are more affordable and family-friendly. However, across the board renters are left with less than half of their pre-tax gross income to pay for bills, taxes, and cost of living, outside of their rent. This makes saving earnings difficult month to month. Renter demographics are aging. Renters are staying longer in their rentals and building families in them, further illuminating the unaffordable nature of home ownership across the country.

In Winnipeg, 21.4% of renters have children, and the city’s renters have the oldest median age in Canada (34.1). This indicates that Winnipeg offers greater affordability for renters seeking to start families.

The traditional model of "rent in 20s, buy before kids" is breaking down - renters are now in their mid-30s, and whether they have families depends more on regional affordability than age.

Rents are exceeding 30% of gross income across most of the country. Currently, Halifax and Montreal tenants face the most affordability strain, seeing lower incomes yet higher rent prices on average. Toronto and Vancouver appear less affordable overall, yet renters have higher incomes on average, which offsets higher rent costs.

Vancouver and Toronto continue to lead as Canada’s most expensive rental markets, while Quebec and the Prairies remain the last bastions of relative affordability.

Higher rents tend to coincide with older renter populations, while provinces with lower rents (like the Prairies and Quebec) see a higher share of households with children.

How to read this chart: Bars show average rent by age group, with darker shades for older renters. The purple line represents the share of households with children, showing where family renters are most concentrated.

Despite regional income differences, renters across Canada face similar affordability pressures. Rent consumes about one-third of household income, and when combined with debt, many households are left with limited disposable income.

How to read this chart: The bar chart shows monthly expenses of rent, debt, and a renter’s income after these expenses are subtracted. The top line number shows the monthly gross household income before taxes. The purple line tracks the rent-to-income ratio, highlighting where housing costs take up more of renters’ pay.

Affordability improves in dual-income households: rent’s share drops by nearly eight points when measured against household rather than personal income, allowing these renters to better absorb high rental costs.

How to read this chart: Each city shows rent as a share of personal income and household income. The gap between the two reflects how renting is more affordable on two incomes instead of one. All income is measured as gross monthly income before taxes.

While over half (53%) of renters earn under $60,000 annually, an increasing share fall into higher income brackets — with many earning well above $100,000. This shift points to a more affluent renter base overall, even as rent continues to consume roughly one-third of household income.

$67,536

$109,056

PERSONAL INCOME

RANGE

SEGMENT SIZE

28.4%

25.1%

19.2%

10.7%

8.1%

3.1%

5.5%

Province

AVG

RENT

MONTHLY INCOME

RTI

B.C

$2,490

$10,460

33.9%

Alberta

$1,869

$9,021

29.6%

Prairies

$1,683

$7,588

30.2%

Ontario

$2,159

$9,233

33.6%

Quebec

$1,623

$7,460

32.9%

Maritimes

$1,890

$8,230

32.6%

CITY

AVG

RENT

MONTHLY INCOME

RTI

Vancouver

$2,891

$12,183

35.6%

Calgary

$2,028

$9,699

27.7%

Winnipeg

$1,713

$8,975

26.0%

Toronto

$2,581

$11,862

30.6%

Montreal

$1,605

$7,479

32.3%

Halifax

$2,145

$9,371

34.2%

On average, renters fall in the good credit range, with a large share in great to excellent. Year over year, we are seeing credit strength improve over time across the provinces, while this trend is reversed in larger cities. Metropolitan renters tend to have better credit suggesting more financially stable renters, compared to rural counterparts. Selecting tenants with proven credit discipline, requiring co-signers, or rent guarantees for weaker profiles can reduce delinquency risk.

693.4

RANK

CREDIT SCORE RANGE

SEGMENT

SIZE

Low

360-559

12.3%

Fair

560-639

14.2%

Good

640-699

20.5%

Great

700-759

24.6%

Excellent

760+

28.4%

city

CREDIT SCORe

yoy

Vancouver

731.1

Calgary

702.8

Winnipeg

654.8

Toronto

732.7

Montreal

688.2

Halifax

705.4

Canada has a favourable rental environment for property owners. Stronger tenant credit health means fewer payment issues, better tenant quality, less turnover, greater retention, and greater financial stability across rental portfolios.

Credit disparities by region suggest landlords in Winnipeg or the Prairies should tighten screening, personalize terms, and maintain financial buffers to offset higher tenant-risk variability.

This could indicate growing financial strain among residents despite high income levels, possibly tied to increased debt loads or cost-of-living pressures. If this trend continues, it may signal emerging credit risk in an otherwise financially stable market.

Although metropolitan cities are more expensive for tenants to afford, we see better quality tenants cluster within them across risk indicators such as collections rates, bankruptcy rates, and average credit scores. Property investors looking to expand their portfolios of income properties should plan strategically. Property prices may be lower in more rural areas, but tenant financial stability and risk increases in those areas as well.

Collections

18.9%

Bankruptcies

3.9%

Credit score

655

Collections

10.1%

Bankruptcies

2.9%

Credit score

703

Collections

7.7%

Bankruptcies

2.1%

Credit score

688

Collections

7.3%

Bankruptcies

2.1%

Credit score

731

Collections

6.7%

Bankruptcies

1.7%

Credit score

705

Collections

4.3%

Bankruptcies

1.1%

Credit score

735

With the lowest delinquency and bankruptcy rates, and maintaining strong credit performance, these cities represent lower payment risk and higher tenant reliability, making them strong rental market opportunities for landlords.

Calgary’s rates indicate higher-than-average debt strain despite relatively solid credit scores, while Montreal’s slightly lower scores and moderate collections suggest income-to-debt imbalances among renters.

Nearly 1 in 5 tenants have accounts in collections and the highest bankruptcy rate among major cities. These trends, coupled with the city’s lower average credit score, suggest significant financial stress and a higher likelihood of missed or late rent payments.