Should your tenant get renters insurance? The answer is a resounding yes. When your tenant has insurance, it benefits you and your tenant. If a fire or natural disaster occurs, your tenant’s insurance can cover all relocation and additional living expenses. Plus, their insurance can compensate for damaged or stolen property up to their policy limit.

Most landlords perceive tenants with renters insurance as safer bets. We’ll explore why most tenants get insurance and why landlords should encourage their tenants to have it.

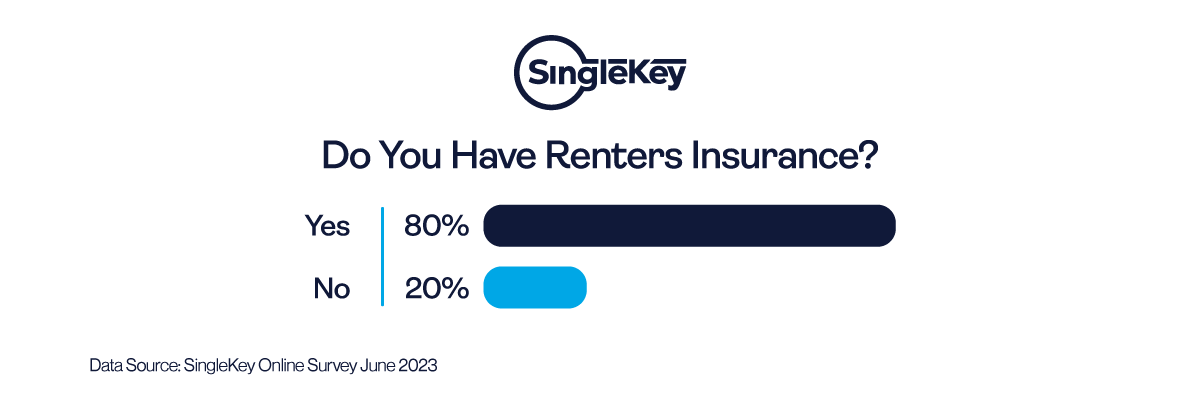

Renters insurance coverage: Does your tenant have it?

SingleKey asked 945 renters if they had renters insurance, and 80% said they did, while only 20% remained uninsured. Many renters misjudge how valuable their belongings are, and when theft or fires occur, everything damaged or stolen is gone, leaving the tenant to rebuild what was lost. With renters insurance, a tenant can feel some consolation that they can rebuild or afford to compensate for their belongings.

While this type of insurance benefits renters the most, there are perks for landlords as well. For instance, landlords can avoid liability claims brought on by tenants due to property damage, like accidental damage caused by cooking fires. If a tenant is insured, the tenant will file a claim, depending on their coverage.

During the screening process, landlords can rest assured that if a tenant’s instinct is to obtain renters insurance on their own, it’s very likely that they will be reliable renters.

Landlord insurance compared to renters insurance policies

Landlord insurance policies have different coverages in comparison to renters insurance policies. Let’s take a look at what each type of policy covers and the benefits to landlords and tenants.

Landlord insurance pros and cons

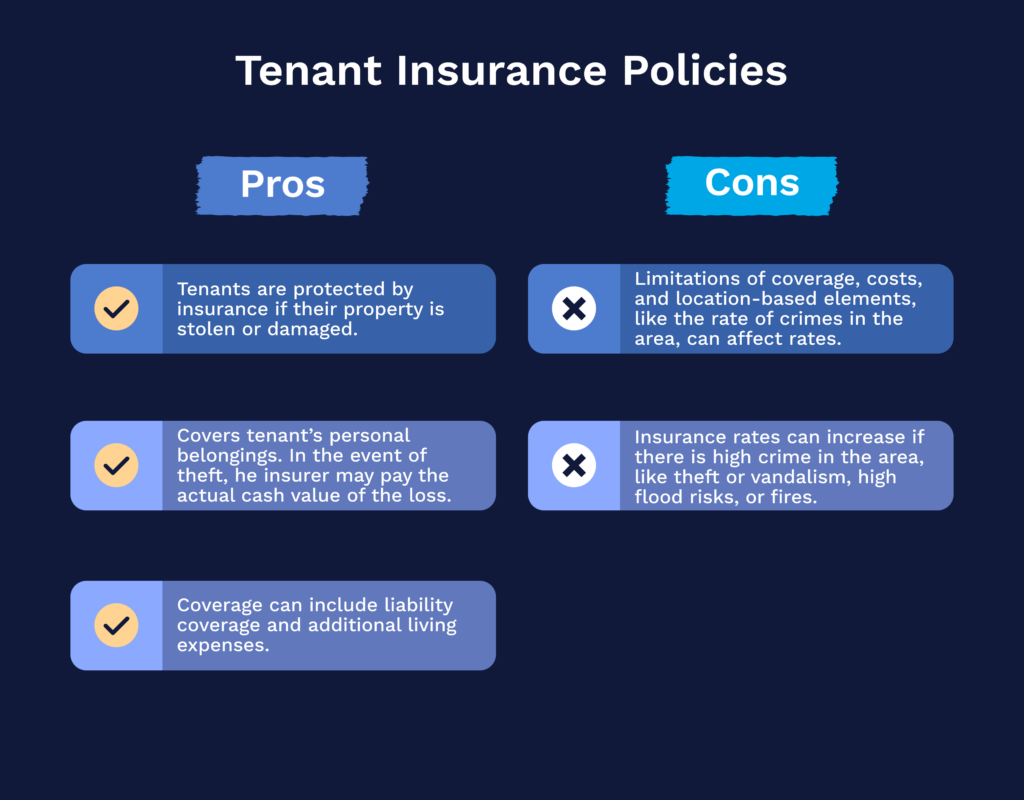

Tenants aren’t legally required to be insured, but landlords and co-ops may require tenant insurance to protect the building or unit. Renters insurance can cover the tenant’s personal belongings in the event of theft or damage inside the property, but it doesn’t cover stolen vehicles. It may cover items stolen within the vehicle up to the policy limits.

There are different types of coverage, and while protecting personal belongings may seem unnecessary initially, it could come in handy one day if a tenant’s bike or work computer gets stolen. While the insurance may not replace what was stolen, it would be able to provide the actual cash value of the item in question.

Many tenants are surprised by how much insurance coverage is available for renters. And the cost of renters insurance rarely exceeds $300 annually. Insurance is relatively inexpensive, depending on environmental factors. It will also offer tenants and landlords peace of mind. Tenant insurance covers:

- Personal property: Insurance will cover costs of repairs or replacement of your personal effects, including furniture, computers, clothes, heirlooms, art, or any specific items listed in a policy.

- Additional living expenses: Hotel accommodations and groceries if the rental is unlivable.

- Liability: If your tenants get liability coverage, their insurance company will cover the medical bills of anyone injured on the rental property. Tenants should ask the insurance company which medical expenses are applicable. Some of the liability coverage (up to the policy’s limits) include:

- Accidental tenant-inflicted flooding

- Water backup by way of sewers and drains

- Pet damage caused by a tenant’s pet

- Some fire damage to property structure*

*Not all liability coverage covers fire damage to structures caused by tenants. Tenants and landlords alike should read through all of the literature on their policies and confirm with their insurance agent what is covered. Renters insurance generally doesn’t cover structural damage to the property. That’s where landlord insurance kicks in.

Can I ask my tenant to pay insurance premiums?

Yes, you can encourage your tenant to get insurance; however, you can not evict them if you ask them during their tenancy and they refuse to get it. Landlords can ask prospective tenants to review different renter’s policies before the move-in date. Making this step a part of the screening and approval process is essential. Some landlords request tenants to have extensive renters policies that include personal property, liability, and additional living expenses. The ideal time to ask your prospective tenant to get renters insurance is:

- During the application process

- In the lease terms

- During the tenancy as a stipulation if the renter decides to get a pet

Analysis of renters insurance, premiums, and deductibles

Tenants should shop around for rates from different insurers. Ideally, they’ll want a comprehensive plan at a low rate. Monthly and annual rates will vary depending on which state your rental is based. For example, in Wisconsin, the average monthly rate is as low as $8 for $15,000 of property coverage, while in Louisiana, the average monthly rate is $25. The wide range of premiums is due to the fact that property crime in Louisiana is high, and in Wisconsin, it’s low. Wisconsin is at low risk for property theft and natural disaster. Because of Louisiana’s proximity to the Gulf of Mexico, it is at high risk for hurricanes and flooding. These contributing factors affect the cost of insurance. Tenants should consider these factors when shopping for renters insurance:

- Coverage options

- Discounts

- Reviews and complaints

- Options for bundling to reduce rates

When your tenant bundles their car insurance with their renters insurance policy, they can lower the cost of their renter and car policies with some insurers.

How do deductibles on renters insurance work?

A deductible is subtracted from the amount of the claim for damaged or stolen items. Like homeowner’s insurance, if a tenant files a claim, the insurer will pay the tenant the remaining amount after the deductible. Hypothetically, let’s say your renter’s $1,500 LG television was stolen, and your tenant’s deductible is $500. The insurance company will subtract the $500 deductible, and the insurance company will pay the tenant $1,000.

Why tenants should have coverage on their rental unit

There are many benefits of renters insurance. Since landlord insurance doesn’t protect your tenant’s personal items, their tenant’s insurance will. Remind your tenant to photograph their valuables once they move into the rental.

When your tenant has liability insurance, it can cover the costs of injuries incurred by a guest and, in some cases, property damage caused by the tenant or guest of a tenant.

The likelihood of a landlord’s premium increasing after filing a claim is very high. If your tenant has personal property coverage and liability insurance, their insurance will cover loss or injury, which will not affect your premium.

FAQ: Why tenants should invest in renters insurance